Martin Marietta Materials: The Rock-Solid Moat of Infrastructure

I. Introduction & The Transformational Blockbuster

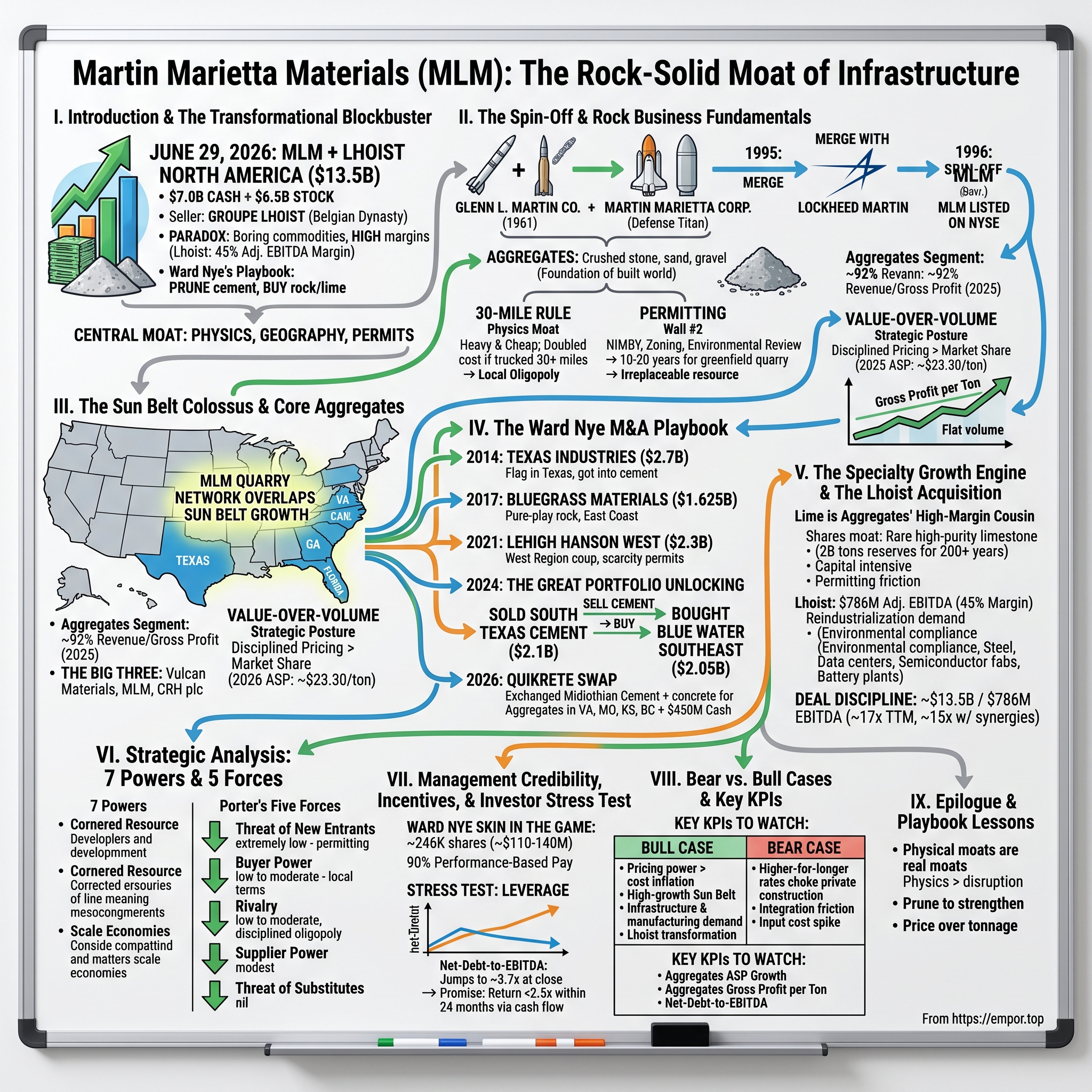

Monday, June 29, 2026 began for Martin Marietta investors the way the most important days usually do: with a press release that re-drew the map. Before the market opened, the Raleigh, North Carolina company announced it had agreed to combine with Lhoist North America — the largest lime and limestone producer in the United States — in a cash-and-stock transaction valued at roughly $13.5 billion.[^1] The structure was $7.0 billion in cash and $6.5 billion in Martin Marietta common stock, the single largest deal in the company's history by a wide margin.[^1]

To understand why this mattered, you have to understand the seller. Lhoist North America is the American arm of Groupe Lhoist, a privately held Belgian industrial dynasty founded in 1889 and controlled to this day by the Berghmans family. They are not a private-equity flipper or a distressed seller. They are old European industrial money — the kind of owner that holds assets for a century and measures returns in generations. And the terms of the deal revealed exactly how they think about value: rather than take all cash and walk away, the Berghmans family agreed to take $6.5 billion of the consideration in Martin Marietta stock, leaving them owning roughly 15% of the combined company at close.[^1] A Belgian limestone family, in other words, will become the single largest shareholder of an American Sun Belt aggregates giant. They are not cashing out of the rock business. They are doubling down on it.

That is the first clue to the central paradox of this entire episode. Martin Marietta digs up, crushes, and hauls the most boring commodities imaginable — stone, sand, gravel, and lime — and yet it generates some of the most consistent, durable, double-digit margins in the global economy. Lhoist itself was the proof point baked into the deal: for the twelve months ended December 31, 2025, Lhoist North America produced $1.8 billion in gross sales and $786 million in adjusted EBITDA — a 45% adjusted EBITDA margin, richer than Martin Marietta's own celebrated aggregates business.[^1] How does crushing rock throw off margins that would make a software founder blush?

The answer is the spine of this story, and it has almost nothing to do with the rock itself and almost everything to do with physics, geography, and permits. Over the next several hours of this episode we will trace four arcs: the strange aerospace lineage that produced an aggregates company; the brutal, beautiful economics of the "30-mile rule" that turns every metropolitan quarry into a local monopoly; the two-decade masterclass in portfolio recycling that current management has run; and the strategic mind of one man — Chairman, President, and CEO Ward Nye — who has spent fifteen years selling cyclical, carbon-heavy cement at the top and buying scarce, high-margin rock and lime for the long haul. The Lhoist deal is not a departure from that playbook. It is its largest single expression.

Let us start at the beginning, which — improbably — is in the sky.

II. The Spin-Off & Rock Business Fundamentals

The name "Martin Marietta" should set off a flicker of recognition for anyone who lived through the Cold War, and it has nothing to do with gravel. To find the origin of this company you have to go back to a barnstorming era of open-cockpit biplanes and a man named Glenn L. Martin, who built airplanes for the U.S. military and once employed both Donald Douglas and a young engineer named William Boeing's contemporaries. His Glenn L. Martin Company merged in 1961 with the American-Marietta Company — a maker of paints, chemicals, and, crucially, construction aggregates — to form Martin Marietta Corporation, a sprawling aerospace-and-materials conglomerate.

For three decades, Martin Marietta was a defense titan: missiles, satellites, the external fuel tank for the Space Shuttle. Then came the great post–Cold War consolidation of the American defense industry. In 1995, Martin Marietta merged with the Lockheed Corporation to create Lockheed Martin, the largest defense contractor on earth. And here is where our company is born, almost as an afterthought. Lockheed Martin had no interest in being in the business of crushed stone. So in 1996, it spun off the aggregates division as a separate, publicly traded company: Martin Marietta Materials, Inc., listed on the New York Stock Exchange under the ticker MLM. The aerospace dynasty kept the rockets. The new company kept the rocks.

It is worth pausing on the strangeness of this lineage, because it shaped the culture. Martin Marietta Materials was not founded by a wildcatting quarry man. It was carved out of a disciplined, engineering-driven defense contractor, and it inherited that temperament: process-oriented, safety-obsessed, allergic to hype. That DNA matters when we get to capital allocation.

Now, what exactly did the new company sell? Aggregates — the industry term for crushed stone, sand, and gravel. If you want a mental image, think of the gray crushed rock under every highway, the sand in every bag of concrete, the gravel under every railroad tie. Aggregates are the literal foundation of the built world. A mile of interstate highway consumes roughly 38,000 tons of the stuff. A single-family home swallows hundreds of tons. There is no substitute — you cannot 3D-print a roadbed or download a foundation. It is the most non-discretionary physical input in the entire economy.

And yet, on a per-unit basis, it is nearly worthless. A ton of aggregates sells for around twenty-odd dollars. Compare that to a ton of, say, copper, which runs into the thousands. This combination — extremely heavy, extremely cheap — is the single most important fact about the entire business, because it creates what is arguably the most underappreciated economic moat in capitalism. Welcome to the 30-mile rule.

Here is the physics. Because aggregates are so heavy and so cheap, the cost of trucking them dominates the economics. Industry rule of thumb: haul a load of rock about 30 miles by truck and you have roughly doubled its delivered cost. Haul it 50 or 60 miles and the freight bill exceeds the value of the rock itself. The product effectively cannot travel. A quarry in suburban Dallas simply cannot compete for a project in suburban Houston — the diesel would eat the margin alive.

What does that do to the competitive landscape? It atomizes it. Every metropolitan market becomes its own isolated island — a local oligopoly, sometimes a local monopoly. If you own a permitted, operating quarry inside a high-growth metro, the laws of physics build a wall around your market that no distant competitor can scale. Your moat is not a brand or a patent. Your moat is freight cost, and freight cost is enforced by gravity.

But there is a second wall, and it may be even taller than the first: permitting. You cannot simply respond to high local prices by opening a new quarry across town. In any built-up American metro, permitting a greenfield quarry takes ten to twenty years, if it can be done at all. The reasons are deeply human. Nobody wants a quarry next door — the blasting, the dust, the truck traffic, the vibration. The acronym is NIMBY, "Not In My Back Yard," and it is the aggregate operator's best friend, because it makes the existing, already-permitted quarry irreplaceable. Layer on zoning fights, environmental review, water-table studies, and noise ordinances, and you arrive at a remarkable conclusion: a permitted, reserve-rich quarry near a growing city is a finite, cornered resource that gets more valuable every year precisely because no one can build a new one.

So the new company that Lockheed Martin tossed overboard in 1996 turned out to be sitting on a collection of legally protected, physically defended local monopolies. The trick of the next thirty years would be figuring out how to own the right ones — and how to charge for them. That is where the story leaves the dusty quarry floor and walks into the war room.

III. The Sun Belt Colossus: Core Aggregates & Competitor Analysis

Picture the geography of American growth over the last two decades as a heat map, and the hottest band runs across the bottom of the country: Texas, Florida, Georgia, the Carolinas. People move there, companies relocate there, highways get built and rebuilt there. Now overlay Martin Marietta's quarry network on that same map, and the two light up in nearly identical shapes. That overlap — not any single clever deal — is the engine room of this company.

Let us size it. In 2025, before a single ton of Lhoist limestone entered the picture, the Aggregates segment generated $5.004 billion in revenue and $1.677 billion in gross profit — roughly 92% of the company's segment revenue and 92% of its gross profit.1 Everything else Martin Marietta does is, financially speaking, a rounding error around the rock. When you analyze this company, you are analyzing an aggregates business with some interesting attachments.

To understand Martin Marietta's place in that business, you need to meet the Big Three of North American aggregates — because this is, fundamentally, a consolidated oligopoly, and the identities of the players tell you how the pricing game gets played.

First, Vulcan Materials Company (NYSE: VMC), the largest pure-play domestic producer and Martin Marietta's closest rival. Vulcan moved roughly 234 million tons of aggregates in a recent year across nearly 400 active facilities — call it the high-single-digit slice of total U.S. volume.6 Vulcan and Martin Marietta are the Coke and Pepsi of American rock, two disciplined operators who learned long ago that beating each other up on price in a shared local market accomplishes nothing.

Second, Martin Marietta itself. In 2025 the company shipped 198.5 million tons of aggregates across roughly 360 active sites.1 Note that this is less volume than Vulcan — and Martin Marietta is, almost by design, content with that. We will come back to why.

Third, CRH plc, the Dublin-headquartered global building-materials giant, whose Americas Materials division pushes well over 200 million tons. But CRH is a different animal: it is heavily integrated downstream into asphalt paving and construction services, so a large share of its rock never gets sold to a third party at all — it gets consumed inside CRH's own paving jobs. That makes CRH both a competitor and, at times, a counterparty, as we will see.7

Around these three orbit the global cement-led players — Heidelberg Materials AG of Germany and Cemex S.A.B. de C.V. of Mexico — who hold meaningful regional positions but whose center of gravity sits in cement, the very business Martin Marietta has spent years trying to exit.

Now, the strategic punchline, and it is the single most important thing to understand about how Martin Marietta runs. The company practices what management calls "value-over-volume." In plain English: it would rather sell fewer tons at a higher price than chase market share by discounting. In 2025, Martin Marietta pushed its aggregates average selling price up roughly 7% to $23.30 per ton.1 That is not an accident of the market; it is a deliberate posture, repeated year after year on earnings calls, of leaning into price even when it means walking away from low-margin volume.

Why does this work? Go back to the 30-mile rule. In a normal commodity, cutting price wins you share from a distant competitor. But in aggregates, there is no distant competitor — the customer physically cannot buy from a quarry 200 miles away. So cutting price does not win you a single incremental ton; it just lowers the price on the tons you were going to sell anyway. Discounting in aggregates is almost pure self-harm. The rational move, in a market where local demand is fixed by local construction activity, is to price for margin and let volume follow the economy. Vulcan plays the same game. The result is an oligopoly that competes on operational excellence and disciplined pricing rather than price wars — which is exactly why these companies earn the margins they do.

What does that disciplined pricing actually buy shareholders? Roughly $8.50 of gross profit on every ton sold in 2025 — a number that has marched steadily upward for years even when volumes were flat or down.1 That is the tell of a high-quality business: profit growth decoupled from unit growth. When a company can grow earnings while shipments stand still, it is harvesting pricing power, not riding a volume cycle.

And the demand backdrop underneath all of this is unusually durable. A large chunk of aggregates demand comes from state departments of transportation and local governments building and repairing roads — spending that is non-discretionary and, since the 2021 federal Infrastructure Investment and Jobs Act, exceptionally well-funded for years to come. Layer the Sun Belt's relentless population and job growth on top of that public-works floor, and you have a demand profile that is both defensive (governments must repair roads in a recession) and growth-levered (people keep moving south). It is a rare combination.

But pricing power and good geography only get you so far if you allocate capital badly. The real story of the modern Martin Marietta — the part that separates it from being merely a well-located quarry company — is what one man chose to buy and, just as importantly, what he chose to sell.

IV. The Ward Nye M&A Playbook: Benchmarking Two Decades of Capital Deployment

If this company has a protagonist, it is Ward Nye. A lawyer by training who came up through the aggregates industry and took the CEO chair in 2010, Nye is not a flamboyant figure. He speaks in the careful, slightly lawyerly cadence of someone who has been deposed before, and he runs the company through a recurring strategic framework he calls SOAR — Strategic Operating Analysis and Review — a multi-year plan he refreshes and reports against with the regularity of a metronome. The substance behind the acronym is a simple, ruthless idea: relentlessly upgrade the portfolio toward scarce, high-margin, low-cyclicality assets, and recycle out of everything else. To see how he does it, walk through the deals in sequence — because the sequence is the strategy.

Texas Industries (2014) — $2.7 billion. This was Nye's first swing-for-the-fences, and it was controversial. Martin Marietta agreed to combine with Texas Industries, a Dallas-based producer, in an all-stock deal announced in January 2014.5 The math looked frightening on the surface: the purchase price worked out to roughly 18.6x trailing EBITDA — a nosebleed multiple. But that headline number was deceptive, because TXI's earnings were sitting in the trough of a vicious post-financial-crisis construction depression. Nye was not paying 18x for a normal year; he was paying a trough multiple on trough earnings, betting that Texas construction would roar back. The deal dragged Martin Marietta into the cement and ready-mix concrete business — which, in hindsight, Nye would spend the next decade unwinding — but it also planted the company's flag in Texas with a portfolio of premium aggregates and the country's most important construction market. The aggregates were the prize; the cement was the price of admission.

Bluegrass Materials (2017) — $1.625 billion. Three years later came a cleaner, more characteristic deal: the purchase of Bluegrass Materials, then the largest privately held pure-play aggregates company in the country.4 The multiple was about 13.3x trailing EBITDA — squarely in line with what premium aggregates assets fetched at the time (Vulcan paid comparable multiples for similar assets). There was no messy cement attached. Bluegrass was pure, high-margin rock, and it thickened Martin Marietta's footprint up the East Coast and into the Mid-Atlantic. If TXI was Nye learning to swing big, Bluegrass was Nye buying exactly the kind of asset he actually wanted: scarce, permitted, aggregates-only reserves near growing markets.

Lehigh Hanson West (2021) — $2.3 billion. Then, in 2021, Nye pried a crown jewel out of Heidelberg Materials AG (then HeidelbergCement). Martin Marietta bought Lehigh Hanson's West Region — 17 active aggregates quarries — for $2.3 billion, valued at roughly 11.8x EBITDA net of acquired tax assets.3 Strategically, this was a geographic coup: it vaulted Martin Marietta into California and Arizona, two enormous, supply-constrained megaregions where permitting a new quarry is somewhere between extraordinarily difficult and politically impossible. In aggregates, the value is in the dirt you are allowed to dig, and Nye had just bought a portfolio of permits that no amount of capital could recreate.

Now comes the part of the playbook that is genuinely distinctive, and it is the inverse of what most empire-building CEOs do. Having spent a decade accumulating, Nye spent 2024 through 2026 aggressively pruning — selling the volatile, capital-intensive, carbon-heavy downstream cement and concrete assets at rich valuations, and rotating the proceeds into more scarce upstream rock. Call it The Great Portfolio Unlocking.

The CRH sale (2024). In early 2024, Martin Marietta sold its South Texas cement plant and associated concrete operations to CRH plc for $2.1 billion in cash.[^5] The disclosed multiple — roughly 12.4x EBITDA — is the tell. Nye sold cement for a 12x multiple, a price that historically would be considered generous for a cyclical, carbon-intensive business that requires constant heavy capital to run a kiln. He was, in effect, selling a lower-quality business at a high-quality price.

The Blue Water acquisition (2024). Almost simultaneously, he redeployed. Martin Marietta announced the $2.05 billion cash purchase of Blue Water Industries' Southeast aggregates operations — adding roughly a billion tons of pure-play reserves in high-growth Southeastern markets.[^6] (In the same window the company also closed the bolt-on acquisition of Colorado's Albert Frei & Sons, deepening its Front Range aggregates position.2) Read the two 2024 moves together and the strategy is naked: sell cyclical cement at 12x, buy scarce rock with the proceeds. Trade a depreciating, carbon-heavy liability for an appreciating, finite asset.

The QUIKRETE swap (2026). The most elegant move came in February 2026, when Martin Marietta completed an asset exchange with Quikrete Holdings.[^3] Rather than sell for cash and pay tax, Nye traded away the Midlothian, Texas cement plant and a package of ready-mix concrete assets — more downstream baggage — in return for aggregates operations spanning Virginia, Missouri, Kansas, and British Columbia, plus $450 million in cash.[^3] He handed Quikrete the carbon-intensive cement it wanted and walked away with more of the scarce rock he wanted and a check on top. It is hard to design a cleaner expression of "prune to strengthen."

Step back and the pattern across fifteen years is unmistakable, and an investor should take it as the core evidence of management quality: Nye buys aggregates at sensible multiples, holds them forever, and treats cement as a trading asset to be sold into strength. Whether every multiple was perfectly timed is debatable — the TXI price still raises eyebrows — but the direction of the rotation has been consistent, disciplined, and aligned with where the durable moats actually live. Which sets up the question of the entire 2026 story: if Nye has been systematically shedding everything that is not high-moat rock, why did he just spend $13.5 billion on lime?

V. The Specialty Growth Engine & The Lhoist Acquisition

For most of its public life, Martin Marietta has had a quirky little third business that analysts barely bothered to model. Tucked behind the aggregates juggernaut sat the Magnesia Specialties segment — a niche operation making high-purity magnesia chemicals and dolomitic lime out of facilities in Michigan and Ohio, selling into flame retardants, wastewater treatment, and steel-making. In 2025 it generated $441 million in revenue and $137 million in gross profit.1 Respectable, high-margin, and utterly immaterial to a company doing six billion dollars in sales. It was the kind of segment you mention on slide 40 and never discuss again.

The Lhoist deal detonates that complacency. Overnight, the specialty business stops being a footnote and becomes a multi-billion-dollar growth engine — and to understand why Nye was willing to write his largest-ever check for it, you have to understand that lime is aggregates' high-margin cousin.

Lime is what you get when you take high-grade limestone and "burn" it in a kiln at extreme temperatures, driving off carbon dioxide to produce quicklime and hydrated lime — versatile alkaline chemicals. Here is the crucial economic point: lime shares the exact same moat structure as aggregates, only more so. It depends on access to rare, high-purity limestone reserves — not the ordinary construction-grade rock that is common, but the chemically pure deposits that are genuinely scarce. Lhoist North America sits on roughly 2 billion tons of premium high-grade limestone reserves, enough for more than 200 years of production at current rates.[^1] And building a new lime kiln is enormously capital-intensive and subject to the same decade-long permitting gauntlet as a quarry. Scarce reserves plus high capital barriers plus permitting friction equals — once again — a cornered resource. Nye was not straying from his playbook. He found a business that runs the identical playbook at higher margins.

How much higher? Recall the headline economics: Lhoist North America's $786 million of adjusted EBITDA on $1.8 billion of gross sales is a 45% margin — meaningfully fatter than even Martin Marietta's vaunted aggregates business.[^1] And the operation is no collection of orphan plants; it comprises roughly 20 quarries and production facilities plus 45 distribution terminals across the United States, with a logistics network that mirrors the kind of river-rail-terminal distribution Martin Marietta prizes.[^1]

But margin alone is not the thesis. The thesis is where the demand comes from — and this is where the deal taps into the single biggest macro story of the decade: the reindustrialization of America. Lime is not primarily a construction product. It is an industrial reagent, and its end markets read like a list of everything the United States is currently scrambling to build. Lime scrubs sulfur out of power-plant flue gas and purifies municipal water (environmental compliance). It is essential to steel-making, where it removes impurities from molten iron. And it is consumed in vast quantities by the construction and operation of the data centers, semiconductor "fabs," and battery plants now rising across the Sun Belt — the very wave of advanced manufacturing that federal industrial policy has been pouring money into. In other words, Nye is positioning Martin Marietta to sell the picks and shovels to the AI-and-onshoring buildout, using a product with a two-century reserve life and a 45% margin. That is the pitch, and it is a genuinely compelling one.

Now the discipline question, because this is the most expensive thing Nye has ever done. At $13.5 billion against $786 million of EBITDA, the deal was struck at roughly 17x trailing EBITDA — and even adjusting for the targeted $85 million of run-rate cost synergies, the multiple lands around 15x.[^1] That is a full price. It is richer than the 11.8x he paid for the Lehigh Hanson quarries and far above the 12x at which he sold cement to CRH. A skeptic is entitled to ask whether Nye, the famously disciplined buyer, paid up at the top of a cycle for an asset levered to an industrial boom that may or may not arrive on schedule.

The bull's rebuttal runs like this: 15x for a 45%-margin business with 200 years of irreplaceable reserves, a Sun Belt footprint that slots cleanly into Martin Marietta's existing geography, and exposure to a secular reindustrialization tailwind is a different proposition than 15x for a cyclical, capital-hungry cement plant. You are paying a premium multiple for a premium, scarcity-protected, long-duration asset — and you are replacing low-margin, high-carbon cement in the portfolio with high-margin, environmentally essential lime. Whether that premium proves wise depends entirely on two things investors cannot yet verify: whether the reindustrialization demand materializes as forecast, and whether a disciplined American operator can integrate a century-old Belgian family business without breaking what made it special. Both are open questions. What is not in question is that the deal is internally consistent with everything Nye has done for fifteen years. He bought the highest-quality version of the only thing he has ever really wanted to own.

That consistency — buying scarce, permitted, freight-protected reserves and pricing them for margin — is what the strategy frameworks are built to test. So let us run Martin Marietta through them formally.

VI. Strategic Analysis: 7 Powers & 5 Forces

Strip away the deal news and the segment tables, and the question an investor actually needs answered is brutally simple: why can't someone else just do this? Hamilton Helmer's 7 Powers framework is the cleanest tool for answering it, and in Martin Marietta's case two of the seven powers do almost all the work.

The first and primary power is Cornered Resource. This is the rare power that fits a business like a glove. A cornered resource is a uniquely valuable asset that you control and others cannot replicate at any reasonable cost — and a permitted, reserve-rich quarry inside a growing metro is the textbook example. The limestone is where geology put it, millions of years ago. The permit was granted in a regulatory environment that no longer exists and will never return. The NIMBY politics that block new entrants protect the incumbent automatically and for free. Martin Marietta's roughly 360 aggregates sites — and now Lhoist's 2 billion tons of high-purity reserves with two centuries of life — are not assets that a well-funded competitor can copy. They are assets that, once gone, are gone. That is what makes the moat structural rather than competitive: it does not depend on Martin Marietta being smarter or cheaper than the next operator, only on it owning the dirt.

The second power is Scale Economies, expressed through logistics. The 30-mile rule says rock cannot travel by truck — but it can travel cheaply by river barge, rail, and deep-water ship. Over decades, Martin Marietta built a proprietary network of inland waterway, rail-served, and coastal distribution terminals that lets it economically move material into markets that have no local stone of their own — Gulf Coast Texas, Florida — and underprice any competitor stuck relying on trucks. This is the one mechanism that lets the company bypass the 30-mile rule rather than merely hide behind it, and it is expensive enough to build that it functions as a scale barrier in its own right. A small operator cannot afford a terminal network; a large one with the right river and port positions can defend it indefinitely.

The other five powers are largely absent, and it is worth being honest about that. There is no network effect (rock does not get more valuable as more people use it), no counter-positioning, no brand premium (a roadbed does not care whose quarry the gravel came from), no patents or process power of consequence, and switching costs are modest. Martin Marietta does not need them. Two structural powers, both rooted in physical reality, are enough to produce the margins we have been describing — which is itself a lesson: a business can be world-class on the strength of just one or two powers if those powers are deep enough.

Now run the same analysis through Porter's Five Forces, and every arrow points the same direction.

Threat of new entrants: extremely low. This is the defining feature of the industry. The combination of decade-plus permitting timelines, outright zoning bans on new quarries in many metros, and the political impossibility of siting blasting operations near homes means that, in most markets, the set of competitors is permanently fixed at whoever already holds permits. New capacity essentially cannot be built where it is most needed. There is no clearer example of a regulatory-and-physical barrier to entry in the public markets.

Bargaining power of buyers: low to moderate. A contractor pouring concrete in Atlanta has no commodity substitute — there is no alternative to aggregates — and, thanks to freight economics, cannot credibly threaten to buy from a quarry two states away. That leaves the buyer largely a price-taker on local terms. The one check on this power is that very large infrastructure projects can occasionally negotiate, and demand can soften in a downturn, but the structural position favors the seller.

Competitive rivalry: low to moderate, and crucially disciplined. In most commodity industries, rivalry is murderous. Here, the oligopoly structure plus the futility of price-cutting (you cannot steal a distant competitor's customer, so a price war just destroys your own margin) produces a stable, almost gentlemanly equilibrium. The top players — Martin Marietta, Vulcan, CRH — compete on operational excellence and pricing discipline, not on slashing prices to win share that physics says they cannot win anyway. The result is the regional margin stability that underwrites the whole investment case.

Supplier power and substitution threat round out the picture and are both modest — the main "supplier" is diesel and energy, which is a real cost-inflation risk we will come to, and the substitution threat for both rock and lime is essentially nil. Add it all up and you have a business sitting in one of the most favorable competitive structures Porter's framework can describe. The risk, therefore, is rarely the moat. The risk is the people running it and the balance sheet they choose to run it with.

VII. Management Credibility, Incentives, & Investor Stress Test

A great moat in the hands of an empire-builder who overpays and over-levers can still destroy value. So the next question is whether the people steering Martin Marietta are aligned with the shareholders who ride along — and here the evidence is reassuringly concrete, though not without a sharp edge of risk attached to this particular deal.

Start with skin in the game. Ward Nye personally owns roughly 246,438 shares of Martin Marietta — a stake worth somewhere in the neighborhood of $110 million to $140 million depending on the day's price, or about 0.41% of the company. That is real, generational wealth tied directly to the stock he manages, not a token grant. And the company's governance reinforces alignment with unusually strict guardrails. Executive ownership guidelines require the CEO to hold stock worth at least seven times his base salary (five times for other named executives) — among the more demanding thresholds in the industry. Executives must retain 50% of the net shares they receive from equity vesting until those ownership targets are met, and the company strictly prohibits hedging and pledging of shares, which closes the loopholes that let some executives quietly de-risk their own exposure while preaching alignment to shareholders.

The pay structure pushes in the same direction. Roughly 90% of the CEO's compensation is performance-based rather than fixed salary, and the largest single component — about 55% — comes in the form of performance share units that vest based on three-year cumulative sales growth and adjusted EBITDA, modified by Martin Marietta's total shareholder return relative to peers. In plain terms: Nye gets paid for compounding the business over multi-year windows and for beating his peer group, not for hitting a single year's number or simply showing up. For long-term fundamental investors, this is close to the design you would draw up yourself — long measurement periods, relative benchmarking, and heavy weighting toward at-risk equity. It does not guarantee good decisions, but it ensures that bad ones cost the decision-maker personally.

Now the stress test — because no responsible analysis of a $13.5 billion acquisition can skip the part where a skeptic pokes the balance sheet. And the obvious place to poke is leverage. Funding $7.0 billion of cash consideration means taking on substantial debt, and the deal pushes Martin Marietta's net-debt-to-EBITDA ratio to roughly 3.7x at close.[^1] For a business with any cyclicality, that is a high number. If a recession hit construction demand at the same moment that interest rates stayed elevated, a 3.7x-levered Martin Marietta would have meaningfully less room to maneuver than the conservatively financed company investors have long admired. A short-seller would frame it bluntly: Nye paid a full multiple for a cyclical-industrial asset and levered up to do it, right as the cycle's direction is uncertain.

The bull's — and management's — answer rests on track record. Nye has done this before. After the $2.3 billion Lehigh Hanson West deal, the company levered up and then de-levered rapidly, using the prodigious and recurring free cash flow that aggregates throw off to pay debt down within roughly two years. Management has guided to a similar path here: a return to below 2.5x net-debt-to-EBITDA within 24 months of closing.[^1] The mechanism is credible because aggregates cash flow is genuinely durable — these are not earnings that evaporate in a downturn — and the Lhoist business adds its own 45%-margin cash stream to accelerate the paydown. The honest investor's posture, though, is to treat the de-leveraging plan as a promise to be verified, not a fact already in hand. Nye has earned the benefit of the doubt with prior cycles; he has not yet earned it on a deal this large.

That tension — proven de-leveraging discipline versus unprecedented deal size — is exactly what analysts pressed on when the deal was unveiled, probing both the pricing elasticity assumptions in the lime business and the integration risk of absorbing a private, family-owned Belgian operation into a public American company. Nye's characteristic response is to retreat to metrics: he tracks and reports gross profit per ton with almost obsessive consistency, and he lays out integration timelines in specifics rather than platitudes. That metric-driven transparency is a point in his favor. But transparency about a plan is not the same as the plan working, and the next two years of leverage prints and synergy capture will be the real referendum on whether this deal was disciplined or a reach.

Which brings us to the two-sided ledger every investor has to weigh.

VIII. Bear vs. Bull Cases & Key KPIs

Lay the cases side by side, because the truth of Martin Marietta is that both are strong, and the gap between them is mostly about the macro environment and one very large new bet.

The bull case rests on the most durable foundation in the analysis: pricing power. Martin Marietta has demonstrated, year after year, that it can raise aggregates prices faster than its costs rise — outpacing diesel inflation, labor inflation, and the general cost creep that erodes weaker businesses. That is the signature of a company harvesting a real moat rather than merely riding a cycle. Stack on top of that the company's heavy exposure to exactly the right geography — the high-growth Sun Belt — and to exactly the right demand drivers: federally funded infrastructure that is non-discretionary, plus the manufacturing-megaproject wave of data centers, fabs, and battery plants. And then add the Lhoist transformation, which converts a sleepy niche segment into a multi-billion-dollar, 45%-margin cash engine pointed straight at the reindustrialization theme. The bull sees a compounding machine: structural pricing power, defensive demand, and a freshly upgraded portfolio of the scarcest assets in industrial America.

The bear case is not about the moat — the bear concedes the moat — but about timing, leverage, and integration. The first fear is "higher-for-longer" interest rates choking off the private side of construction. Public infrastructure spending is well-funded and rate-insensitive, but private commercial and residential building is highly rate-sensitive, and a prolonged period of expensive money could push aggregates volumes down even as DOT work holds up. The second fear is integration friction: Lhoist is a 130-year-old, privately held, family-run Belgian business with its own culture and systems, and merging it into a public American operator at the very moment the balance sheet is stretched to 3.7x leverage invites delayed or disappointing synergy capture. The third fear is input costs — a sharp spike in diesel or kiln energy that, for once, outruns Martin Marietta's ability to pass it through on price. Each of these is plausible, and the leverage taken on for the Lhoist deal magnifies the cost of being wrong about any of them.

The synthesis for a long-term investor is that Martin Marietta is a structurally advantaged business making a large, full-priced, debt-funded bet at a moment of genuine macro uncertainty. The quality of the underlying assets is not really in dispute. What is in dispute is whether the price paid for Lhoist and the leverage taken to pay it will look prudent or aggressive when the cycle turns. That is a question only time and execution can answer — which is precisely why the next two years of operating data matter so much.

So what should an investor actually watch? Three KPIs cut through the noise.

First, aggregates average selling price growth. This is the purest read on whether the pricing-power thesis still holds. The relevant question each year is whether ASP keeps climbing in the mid-to-high single digits — roughly the +6% to +8% range the company has been delivering. If price increases stall or reverse, the entire bull case weakens at its foundation, because everything else in the story ultimately rests on Martin Marietta's ability to charge more for the same rock.

Second, aggregates gross profit per ton. Price is only half the equation; this metric captures whether pricing is actually outrunning cost inflation. Gross profit per ton sat around $8.50 in 2025, and the question is whether it pushes above $9.00 and keeps climbing. A rising gross-profit-per-ton in a flat-volume year is the single clearest signal that the company is compounding on quality rather than quantity — the exact behavior that makes this business special.

Third, net-debt-to-EBITDA. This is the referendum on the Lhoist deal and on management's credibility. The number jumps to roughly 3.7x at close, and management has promised to bring it back below 2.5x within two years. Watching that trajectory quarter by quarter is the cleanest way to judge whether Nye's celebrated de-leveraging discipline holds at a scale he has never attempted before. If the line bends down on schedule, the deal looks vindicated. If it stalls, the bear case has its opening.

IX. Epilogue & Playbook Lessons

There is a delicious irony at the center of this entire story. In an era that lionizes the asset-light, the digital, and the infinitely scalable, one of the most reliable long-term compounders in the public market is a company whose core competency is blowing up hillsides and hauling the pieces less than thirty miles. Martin Marietta out-earns, out-margins, and out-durables a great many software businesses not despite the physical heaviness of its product but because of it. The very weight that makes rock worthless to ship is what makes the quarry that owns the local market unassailable. The moat is gravity itself.

Three lessons fall out of the saga for anyone who allocates capital.

The first is that physical moats are real moats. In a culture obsessed with disruption, it is bracing to remember that some advantages cannot be coded around. No app, no algorithm, no clever business model can manufacture a permitted limestone deposit inside a growing city, or repeal the freight economics that protect it. Structural, localized monopolies built on weight, geology, and permitting are precisely the kind of advantage that software cannot touch — and they tend to get stronger with time as new supply becomes ever harder to permit.

The second is prune to strengthen. The most impressive thing Ward Nye did over fifteen years was not buying — anyone can buy. It was the discipline of selling mature, cyclical, capital-hungry cement assets at rich multiples and rotating the cash into scarce, high-margin, long-duration rock and lime. Great capital allocation is as much about what you are willing to let go of at the top as what you are willing to acquire. Nye treated cement as a trading asset and aggregates as a permanent one, and the portfolio he leaves is dramatically higher quality for it.

The third, and perhaps the most broadly useful, is price over tonnage. A business that can grow its profits while its physical volumes sit flat is telling you something profound about its quality: it possesses genuine pricing power, the rarest and most valuable attribute a company can have. Value-over-volume is not a marketing slogan at Martin Marietta; it is the operating philosophy that turns a commodity into a compounding machine.

Whether the $13.5 billion Lhoist bet ultimately ranks alongside Nye's best moves or among his most expensive will not be settled for years. The leverage is real, the multiple is full, and the reindustrialization demand that justifies it remains a forecast rather than a fact. But the bet is, unmistakably, of a piece with everything that came before: a disciplined buyer paying up for the single highest-quality version of the only thing he has ever truly wanted to own — scarce, permitted, freight-protected reserves, priced for margin and held for the long run. A Belgian limestone dynasty, by taking 15% of the company in stock rather than cash, cast its vote that the bet is sound. The market will spend the next decade deciding whether they were right.

References

-

Martin Marietta Reports Fourth-Quarter and Full-Year 2025 Results — Martin Marietta Materials, Inc. / GlobeNewswire, 2026-02-11 ↩↩↩↩↩

-

Martin Marietta Completes Acquisition of Albert Frei & Sons, Inc. — Martin Marietta Materials, Inc., 2024-01-16 ↩

-

Martin Marietta Announces Acquisition of Lehigh Hanson's West Region — Martin Marietta Materials, Inc., 2021-05-24 ↩

-

Martin Marietta Announces Acquisition of Bluegrass Materials — Martin Marietta Materials, Inc., 2017-06-26 ↩

-

Martin Marietta and Texas Industries Agree to Combine — Martin Marietta Materials, Inc., 2014-01-28 ↩

-

Vulcan Materials Investor Relations — Vulcan Materials Company ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube