Figma: The Browser-Based Decade and the $20B "No-Go"

I. Introduction: The $20 Billion "Vibe Check"

🎙 The Hook: The Day the Deal Died

On December 18, 2023, two of the most powerful companies in creative software issued a joint statement that reverberated through Silicon Valley, Wall Street, and every design studio on the planet. Adobe and Figma were calling it off. The proposed $20 billion acquisition—the largest software deal of its kind—was dead. Not because the companies changed their minds. Not because the financials fell apart. Because regulators in the United States, the European Union, and the United Kingdom collectively decided that letting the incumbent swallow its most dangerous challenger would kill innovation in an industry that touches every screen, every app, and every digital experience on Earth.

Figma walked away from the wreckage with something extraordinary: a $1 billion reverse breakup fee, paid by Adobe for failing to close the deal. One billion dollars, wired into the account of a company with roughly 1,900 employees and an annual run rate that had just crossed $600 million. Think about the math on that for a moment. The breakup fee alone represented nearly two full years of operating expenses. It was, in the words of one venture capitalist, "the greatest consolation prize in the history of technology M&A."

But here is the part of the story that most people missed. Dylan Field, Figma's co-founder and CEO, did not look like a man who had just lost a $20 billion payday. He looked like a man who had been let out of a cage. Within weeks of the deal's termination, Figma began hiring aggressively, accelerating product development, and laying the groundwork for what would become the most anticipated technology IPO of 2025. The message was unmistakable: Figma was not a company that needed to be acquired. It was a company that needed to be unleashed.

The thesis of this deep dive is deceptively simple. How did a "toy" built in a web browser by two college dropouts become the System of Record for the entire digital economy? How did a tool that venture capitalists initially dismissed as "Photoshop in Chrome" grow into a platform that ninety-five percent of the Fortune 500 now depends on? And how did the failed Adobe merger—far from being a setback—become the defining catalyst that transformed Figma from a design tool into something far more ambitious: a Product Operating System that serves not just designers, but developers, product managers, marketers, and executives?

The roadmap of this story runs from a dorm room at Brown University to the trading floor of the New York Stock Exchange, where Figma listed under the ticker FIG in July 2025. It passes through years of silent technical development, a brutal competition with desktop incumbents, the most scrutinized software acquisition attempt since Microsoft-Activision, and a post-independence product explosion that has expanded Figma's addressable market by an order of magnitude. Along the way, the story reveals a "hidden business" that most observers still underestimate—the pivot from serving five million designers to capturing fifty million developers, and the AI-powered tools that could redefine what it means to build digital products entirely.

To understand how Figma got here, one must go back to the beginning—to a twenty-year-old named Dylan Field, a fellowship from Peter Thiel, and a technical gamble that everyone said was impossible.

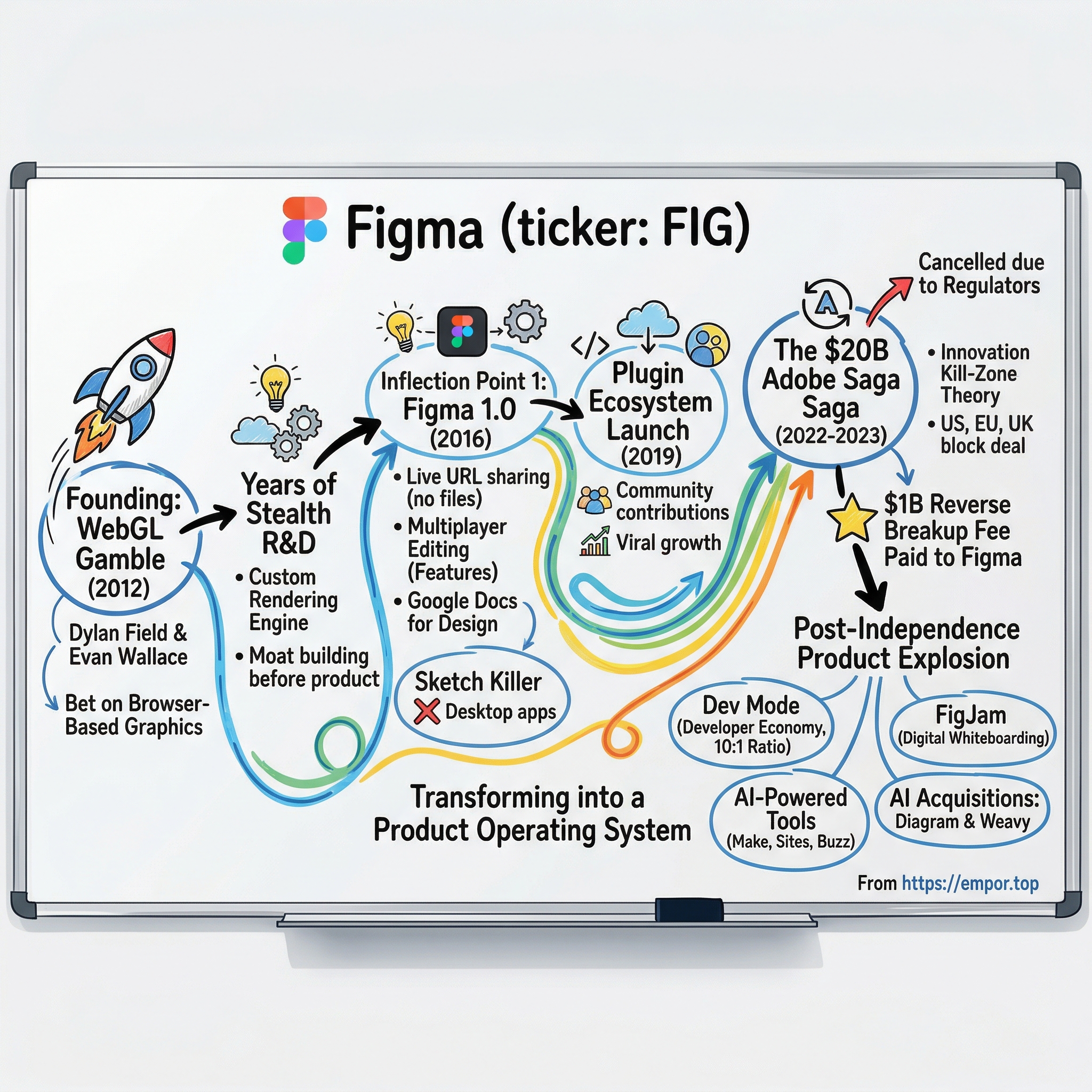

II. Founding Context: The WebGL Gamble

🎙 The Peter Thiel Fellowship and the Impossible Bet

In the spring of 2012, Dylan Field was a sophomore at Brown University studying computer science. He was twenty years old, the only child of a respiratory therapist father and a resource specialist teacher mother, raised in the small town of Penngrove in Sonoma County, California. Field had learned algebra at age six and attended a magnet school on the campus of Sonoma State University for high school. He was, by every measure, the kind of student who was supposed to finish his degree, join a prestigious company, and climb the ladder. Instead, he applied for the Thiel Fellowship—Peter Thiel's provocative program that paid young people $100,000 to drop out of college and build something.

Field won the fellowship and left Brown. His co-founder, Evan Wallace, was a fellow Brown computer science student who had been studying graphics programming and working as a teaching assistant. Wallace finished his degree that spring and joined Field in San Francisco in the summer of 2012. The two of them had a vision that sounded, to most people who heard it, somewhere between naive and delusional: they were going to build a professional-grade graphics editor that ran entirely in a web browser.

To appreciate why this was considered impossible, one needs to understand the state of browser technology in 2012. Web browsers were designed to display text, images, and simple animations. The idea of running a complex vector graphics editor—the kind of software that Adobe had spent decades perfecting as a native desktop application—inside a browser tab was roughly equivalent to suggesting you could run a Formula 1 engine inside a lawnmower. The rendering power simply was not there. Browsers choked on complex visual operations. Latency was unacceptable. The user experience would have been painful.

But Field and Wallace had spotted something that almost no one else in the design-tool world was paying attention to: WebGL. WebGL, which stands for Web Graphics Library, was a relatively new JavaScript API that allowed browsers to render complex two-dimensional and three-dimensional graphics using the computer's GPU—the same graphics processing unit that powers video games. It was a nascent standard, still buggy and inconsistently supported across browsers, but it represented a fundamental shift in what was possible inside a browser window. Field's insight was that WebGL would improve rapidly, and that whoever built the first serious creative tool on top of it would have a massive first-mover advantage.

This was the "Why Now?" question that every great startup must answer. The technology to build professional graphics in a browser had not existed in 2010. By 2012, it was just barely possible. By 2015, it would be good enough to ship. Field and Wallace were betting on a curve, not a snapshot.

What followed was one of the most remarkable periods of silent technical development in recent startup history. For more than three years—from mid-2012 through late 2015—Figma operated in near-total stealth. Wallace built a custom rendering engine from scratch in WebGL, optimizing it for the specific demands of vector graphics editing. This was not a weekend project. This was the kind of deep, painstaking engineering work that most Silicon Valley startups, obsessed with "ship fast and break things," would never have the patience for. Field and Wallace were building a technical moat before they had a product, before they had users, before they had a single dollar of revenue.

The early years were not glamorous. Field, barely out of his teens, had no management experience. He later described himself candidly as "not a very good manager" during this period. Employees grew frustrated. People quit. At one point, according to Field's own account, senior team members staged what amounted to a managerial intervention, telling the young CEO he needed to change his approach. Field took a few days away from the office, sought coaching, and came back different. It was the first of several moments where Field demonstrated an unusual quality for a founder: the willingness to be told he was wrong and the discipline to actually change.

Fundraising was equally challenging. When Field pitched investor John Lilly at Greylock Partners, Lilly initially declined, telling him bluntly: "I don't think you know what you're doing yet." Field refined his pitch, improved the product, and came back. Lilly eventually led Figma's $14 million Series A in December 2015. But the earliest bet came from Danny Rimer at Index Ventures, who led the $3.8 million seed round in June 2013. Rimer reportedly called Field back the same night after hearing the pitch—a vote of confidence that would ultimately generate approximately a ninety-times return when Figma went public.

During the stealth years, Field and Wallace experimented with several concepts—software for drones, a meme generator, 3D content creation, photo editing—before arriving at the idea that would define the company. The original pitch was essentially "Photoshop in the browser," a direct assault on Adobe's flagship product. But as they built and tested, the founders realized something more profound. The browser was not just a different delivery mechanism for the same product. It was a fundamentally different paradigm. If designs lived in the browser, they did not need to be saved as files. If they did not need to be saved as files, they did not need to be emailed, uploaded, or synced. And if multiple people could access the same browser URL simultaneously, they could edit the same design at the same time.

The pivot was subtle but seismic. Figma was no longer "Photoshop in the browser." It was "Google Docs for Design." That single conceptual shift—from a tool you use alone to a place where teams collaborate in real time—would prove to be worth tens of billions of dollars. But first, Figma had to prove it could actually work. And that meant taking on the reigning champion of interface design: a beloved Mac-only app called Sketch.

III. Inflection Point 1: The "Sketch" Killer and The Multi-player Era

🎙 The Desktop vs. Browser War

Picture a product designer at a mid-size tech company in 2015. She works on a Mac, because Sketch—the tool that displaced Photoshop for UI design—only runs on macOS. She finishes a screen design, exports it as a PNG, uploads it to Dropbox, posts the link in Slack, and waits. Her developer colleague downloads the file, opens it, realizes the fonts are missing because he is on Windows, messages her back, she re-exports as a PDF, he downloads again, and by now thirty minutes have passed and the actual design feedback has not even started. If a third colleague needs to make a small tweak, the entire cycle repeats. Version control is a nightmare of files named "homepage_v3_FINAL_actually_final_v2.sketch."

This was the reality of professional design collaboration before Figma, and it was maddening. Sketch was a genuinely excellent design tool—lightweight, fast, purpose-built for interface design in a way that Photoshop never was. It had earned the loyalty of hundreds of thousands of designers who had migrated from Adobe's bloated Creative Suite. But Sketch had a fatal architectural limitation: it was a desktop application, locked to the Mac, and every act of collaboration required exporting, syncing, and re-importing files through third-party services.

Figma launched its free invite-only preview in December 2015 and shipped its first public release, Figma 1.0, in September 2016. The initial product was deliberately simple—a vector editing tool with components that lived entirely in the browser. But the magic was not in any single feature. The magic was in the URL. A Figma design was a live document accessible from any browser on any operating system. When a designer shared a Figma link, the recipient did not download anything. They simply clicked and saw the design, live, in their browser. If the designer made a change, the recipient saw it instantly. There was no file, no export, no sync. The file, as a concept, had been deleted.

This alone would have been compelling. But Figma's true breakthrough was multiplayer editing. From its public launch, Figma allowed multiple people to work on the same design simultaneously, with each person's cursor visible and labeled with their name. It was the Google Docs experience applied to visual design—and it was transformative. Suddenly, a designer and a product manager could be in the same Figma file at the same time, pointing at elements, making changes, leaving comments. Design reviews that previously required scheduling a meeting, projecting a static screen, and talking through exported images could now happen asynchronously, in real time, across time zones.

The technical implementation was sophisticated. Rather than using Operational Transforms—the complex algorithm that powers real-time collaboration in Google Docs—Wallace and the Figma engineering team built a custom syncing system optimized for the specific demands of visual editing. Changes from each user were sent to a central server and broadcast to all other participants in real time. When two users edited the same property on the same object simultaneously, the system applied a "last write wins" rule—simple, predictable, and fast enough that conflicts were vanishingly rare in practice.

Multiplayer was not just a feature. It was a cultural shift. Before Figma, design was an inherently solitary activity. A designer went into a room, created something, and emerged with a finished artifact. The design process was opaque to everyone else on the product team. Figma made design visible, collaborative, and social. Product managers started living in Figma files. Engineers started inspecting designs directly instead of waiting for handoff documents. Executives started dropping into files to see progress. The metaphor shifted from "the designer's workshop" to "the team's war room."

Sketch, to its credit, recognized the threat and began adding collaboration features, including a web-based inspector and cloud-hosted files. But it was retrofitting collaboration onto a desktop architecture, and the experience never matched the seamlessness of a browser-native tool. By 2017, when Figma shipped team libraries—shared component systems that could be maintained centrally and used across an entire organization's design files—the writing was on the wall. Figma was not just matching Sketch feature for feature. It was building a fundamentally different kind of product.

Then came the plugin ecosystem. In August 2019, Figma launched its plugin platform with forty vetted plugins. Within six months, there were 430. The top plugin, Unsplash (which let designers pull stock photos directly into their designs), had over 103,000 installs. Microsoft contributed Content Reel, which generated realistic placeholder data. The ecosystem grew to thousands of plugins, each one extending Figma's functionality without Figma's engineering team writing a single line of the plugin code.

In Hamilton Helmer's framework of competitive strategy, this was "Install-base Power" in its purest form. Every plugin built on Figma's platform made Figma more valuable to its users and simultaneously raised the switching cost of leaving. A design team with dozens of custom plugins, shared component libraries, and years of design history stored in Figma files was not going to switch to a competitor because the competitor had a slightly better pen tool. The ecosystem was the moat.

By 2021, Figma's dominance was essentially complete. Industry surveys showed Figma commanding an estimated eighty to ninety percent market share in the UI and UX design space. Sketch retained over a million users but was increasingly a legacy choice. Adobe, watching from the sidelines, had attempted its own competitive response—a product called Adobe XD—but the effort was halfhearted, the product underfeatured, and the adoption anemic. The giant of creative software was losing a market it should have owned, and losing it to a company that had been founded in a San Francisco apartment by two kids who had just left college.

Something had to give. And in September 2022, it did—in the form of the largest acquisition offer in the history of design software.

IV. M&A Analysis: The Adobe Saga and Capital Deployment

🎙 The $20 Billion Bid

On September 15, 2022, Adobe announced that it had agreed to acquire Figma for approximately $20 billion in a combination of cash and stock. It was Adobe's largest acquisition ever—by a staggering margin. The previous record had been the $4.75 billion purchase of Marketo in 2018. This deal was more than four times larger. The market's reaction was swift and brutal: Adobe's stock fell seventeen percent in a single day, wiping out roughly $30 billion of shareholder value. Wall Street was not questioning whether Figma was worth $20 billion. It was questioning whether Adobe was admitting that its own products could not compete.

To understand the math, consider the metrics at the time of the announcement. Figma was generating approximately $400 million in annual recurring revenue. A $20 billion price tag meant Adobe was willing to pay roughly fifty times ARR—a multiple so extreme that it had virtually no precedent in enterprise software M&A. For context, when Salesforce acquired Slack in 2021 for $27.7 billion, Slack had roughly $900 million in ARR, putting the deal at approximately thirty times revenue. When Facebook acquired WhatsApp in 2014 for $19 billion, WhatsApp had negligible revenue but two billion users. The Figma deal was in the rarefied company of acquisitions where the buyer is not purchasing current earnings but future market dominance.

Adobe's logic, though expensive, was internally consistent. The company's own competitive product, Adobe XD, had failed to gain meaningful traction despite years of investment. Figma was not just winning the market—it was defining an entirely new category of collaborative design that Adobe's desktop-centric architecture could not replicate. If Adobe did not buy Figma, it faced the prospect of watching its most valuable franchise—the creative professional market—migrate to a browser-based platform it did not own. The $20 billion was not a premium for a product. It was an insurance policy against obsolescence.

But the deal never closed. Within weeks of the announcement, regulatory scrutiny began mounting. The U.S. Department of Justice opened a formal investigation in November 2022. The European Commission announced its own review in February 2023, examining whether the merger would reduce competition in the digital design tools market. The UK's Competition and Markets Authority launched a parallel inquiry. The core argument from regulators was what legal scholars call the "Innovation Kill-Zone" theory: that allowing a dominant incumbent to acquire its most innovative challenger would eliminate the competitive pressure that drives innovation, even if the two companies' current product lines did not perfectly overlap.

Adobe and Figma fought the regulatory battle for over a year. Adobe offered concessions. Figma's lawyers presented economic analyses. But the headwinds proved insurmountable. On December 18, 2023, the two companies jointly announced the termination of the merger agreement, stating there was "no clear path to receive necessary regulatory approvals" from the European Commission and the UK CMA. Adobe paid Figma the $1 billion reverse breakup fee stipulated in the merger agreement.

The termination was a watershed moment for the technology industry, extending well beyond Figma and Adobe. It signaled that global regulators—particularly in the EU and UK—were willing to block acquisitions not just on the basis of existing market overlap, but on the basis of potential future competition. For Figma specifically, it was transformative. The company emerged from a fifteen-month regulatory limbo with $1 billion in fresh cash, no acquirer dictating its roadmap, and a renewed mandate to build independently.

How Figma deployed that capital tells you everything about the company's ambitions. Rather than hoarding the breakup fee as a war chest, Field and his team channeled it directly into research and development. The eighteen months following the deal's termination saw an extraordinary burst of product development. Dev Mode launched in beta. AI features were accelerated. The Diagram acquisition brought specialized AI talent in-house. And the company began quietly preparing for what the breakup fee had made both possible and necessary: an initial public offering that would give Figma the permanent capital base to compete against Adobe, Google, and every AI startup gunning for its market.

The irony of the failed acquisition is now visible in the stock market. As of late March 2026, Figma's market capitalization sits at approximately $11.5 billion—roughly the same amount that Adobe was willing to pay for the company in 2022, before the regulatory fight, before the IPO, and before a year of brutal post-IPO stock decline. Whether the current market is right and Adobe was wrong, or whether the market is undervaluing a company that now generates over $1 billion in annual revenue, is one of the most interesting questions in software investing. But the failed deal itself accomplished something that no amount of product development could have: it established Figma's strategic value at $20 billion in the minds of every investor, every competitor, and every employee who now holds FIG stock.

V. Management: The Dylan Field Era

🎙 From Teenage Prodigy to Post-M&A Wartime CEO

There is a particular kind of Silicon Valley founder story that borders on mythology—the wunderkind who builds a billion-dollar company before they are old enough to rent a car. Dylan Field's version of this story is notable for how thoroughly it departs from the archetype. Yes, he dropped out of an Ivy League school at twenty. Yes, he won the Thiel Fellowship. But Field's defining characteristic is not precocity. It is self-awareness—a quality far rarer and far more valuable in a founder than raw intelligence.

Field grew up in rural Sonoma County, the only child of working-class parents. He was not the product of privilege or Silicon Valley connections. His father was a respiratory therapist; his mother was a resource specialist teacher. He learned algebra at six—not because he was pushed, but because he was curious. He attended Technology High School, a magnet school on the Sonoma State campus, where he developed an early facility with computers. At Brown, he chaired the Computer Science Departmental Undergraduate Group and interned at LinkedIn and Flipboard. These were not trivial internships for a college student. They gave Field direct exposure to how large-scale software companies operated, what their design workflows looked like, and where the friction points were.

But what makes Field genuinely unusual is his reaction to failure. When his early employees grew frustrated with his management—or lack thereof—and staged an intervention, Field did not dig in or blame others. He took time away, sought coaching, and fundamentally changed how he led. When John Lilly at Greylock told him he did not know what he was doing, Field did not write him off. He improved his pitch and came back. When the Adobe deal fell apart after fifteen months of uncertainty, Field did not sulk or coast. He accelerated. This pattern—absorb the criticism, adjust, come back stronger—has been the throughline of his entire career.

Field's leadership of post-merger Figma has been what venture investors call a "wartime CEO" performance. In the eighteen months between the deal's termination and the IPO, Figma launched more products and features than in any comparable period in its history. Config 2024, the company's annual conference in June 2024, saw the introduction of Figma Slides (a presentation tool), major AI features powered by third-party models including OpenAI, and a broad expansion of Dev Mode. Config 2025, held at San Francisco's Moscone Center with 8,500 in-person attendees, was even more ambitious: Figma Sites (an AI-driven website builder), Figma Make (prompt-to-prototype powered by Anthropic's Claude), Figma Buzz (marketing content creation), and Figma Draw (vector illustration competing directly with Adobe Illustrator). In October 2025, Figma acquired the Israeli AI startup Weavy for over $200 million, rebranding it as Figma Weave and opening a new R&D center in Tel Aviv.

This product velocity is inseparable from Field's management philosophy. He is known for reading customer support tickets personally, for visiting users in far-flung locations—including Ukraine and Nigeria during the COVID pandemic—and for obsessing over the details of product experience in a way that recalls Steve Jobs's famous attention to what happens inside the box. "Have fun" is one of Figma's three core values, reportedly added by Field after he recognized that the company's early culture was too intense and too joyless. It is a small detail, but it reveals something important: Field understands that a creative tools company that is not itself creative is a contradiction in terms.

On the governance side, Figma's IPO in July 2025 established a dual-class share structure that gives Field extraordinary control over the company's direction. Class A shares, held by public investors, carry standard voting rights. Class B shares, held by Field and a small group of insiders, carry super-voting rights. The result is that Field controls approximately seventy-five percent of total voting power despite holding a roughly ten to seventeen percent economic stake (the exact figure varies by calculation method and filing date). Co-founder Evan Wallace, who departed Figma around 2021 after nearly a decade as CTO, holds shares through a family trust, but Field controls the voting rights on those shares as well.

This structure is controversial—dual-class shares always are—but it serves a specific strategic purpose for Figma. It means that no hostile acquirer, no activist investor, and no short-term-oriented shareholder can force Field to sell the company, change its strategy, or cut R&D spending to boost quarterly earnings. Given that Figma's entire story is built on long-term technical bets that took years to pay off, this protection is not merely a founder's vanity. It is an architectural feature of the company's ability to invest patiently.

For investors evaluating FIG, the management question is straightforward: you are betting on Dylan Field. His track record of building through adversity, his demonstrated ability to learn and adapt, and his structural control of the company's direction make him the single most important variable in Figma's future. The equity pool under the FIG ticker is designed to attract and retain the kind of specialized engineering talent that might otherwise leave to found their own companies. Field has spoken publicly about his "bias" for hiring young workers who are "AI natives," and Figma has been actively hiring—not cutting—in response to the AI revolution. As of early 2026, the company has roughly 1,900 employees, a lean headcount for a company generating over $1 billion in annual revenue.

The question that hangs over Field's leadership is whether the skills that built Figma from zero to one—deep technical vision, long-term patience, user obsession—are the same skills needed to navigate the company through its next phase: a public company facing margin compression, AI disruption, and a stock price that has fallen eighty-five percent from its post-IPO high. The early evidence suggests that Field is adapting once again, but the test is far from over.

VI. The "Hidden" Businesses: FigJam, Dev Mode, and the AI Pivot

🎙 Segment 1: The Developer Economy and The 10:1 Ratio

There is a number that Figma's leadership returns to again and again in investor presentations, and it is the key to understanding why the company believes its best growth is still ahead: for every designer in a typical technology company, there are roughly ten developers. Figma built its business by becoming indispensable to designers. But designers represent a total addressable market of perhaps five million professionals worldwide. Developers number closer to fifty million. If Figma can become a tool that developers use daily—not just occasionally, and not just to inspect someone else's work—the revenue opportunity expands by an order of magnitude.

Dev Mode, launched in beta at Config 2023 and moved to paid tiers in early 2024, was Figma's first serious bid for this expanded market. At its core, Dev Mode transforms the Figma interface for the developer's perspective. Instead of seeing a design canvas, a developer sees code snippets, asset dimensions, spacing values, design tokens, and direct links to code documentation and project tickets. It bridges the historically painful "design-to-development handoff"—the moment when a finished design must be translated into working code—by making the design file itself the source of truth for implementation details. Figma also released a plugin for Visual Studio Code, the most popular code editor in the world, allowing developers to reference Figma designs without leaving their development environment.

The pricing tells the story of Figma's ambition. Dev Mode seats cost $25 per month on Organization plans and $35 per month on Enterprise plans. These are not designer seats being upsold. These are entirely new seats sold to an entirely new user base within the same organization. If a company has fifty designers and five hundred developers, and even a fraction of those developers adopt Dev Mode, the revenue from developer seats dwarfs the revenue from designers. This is the "hidden business" that makes Figma a developer company, not just a design company.

🎙 Segment 2: FigJam and The Office Suite for Product Teams

FigJam launched in April 2021 as Figma's entry into digital whiteboarding—a market that Miro (valued at $17.5 billion at its peak) and Mural had pioneered. On the surface, FigJam looks like a simple product: sticky notes, drawing tools, emojis, voting, timers. But its strategic significance is far greater than its feature list suggests.

FigJam represents Figma's horizontal expansion beyond design entirely. It is used for brainstorming sessions, sprint planning, retrospectives, user journey mapping, and workshop facilitation—activities that involve every member of a product team, not just designers. In June 2022, Figma partnered with Google for Education to bring FigJam to Chromebooks, introducing the tool to students who may never become designers but who will someday run product teams. In November 2023, FigJam gained AI-powered features including content generation and summarization, moving it from a blank canvas to an intelligent workspace.

The strategic logic is the "Office Suite for Product Teams" thesis. Microsoft built a trillion-dollar franchise by putting Word, Excel, and PowerPoint on every desk in every office. Figma's equivalent vision is to put Figma (design), FigJam (collaboration), Figma Slides (presentations), and Dev Mode (development) on every screen of every product team. Each product serves a different function, but they share the same underlying platform, the same user accounts, the same component libraries, and the same collaborative infrastructure. Once a team is using two or three of these products, the switching cost of leaving Figma for any individual tool becomes almost insurmountable.

The May 2025 Config announcements—Figma Sites, Figma Make, Figma Buzz, and Figma Draw—dramatically accelerated this expansion. Figma Sites, powered by AI, allows users to build production websites and web applications directly from Figma designs, complete with a content management system. Figma Make, powered by Anthropic's Claude model, generates functional prototypes from natural language prompts. Figma Buzz creates marketing assets. Figma Draw competes directly with Adobe Illustrator for vector illustration. Each of these products pushes Figma further beyond its design-tool origins and deeper into the workflows of developers, marketers, and content creators.

🎙 Segment 3: AI Acquisitions and the Automation of Design

The AI dimension of Figma's strategy began in earnest in June 2023, when the company acquired Diagram, a startup that had built AI-powered design tools including a product called Magician that could generate UI elements from text descriptions. Diagram's team, led by founder Jordan Singer, was integrated into Figma's core product organization, and their technology formed the foundation of the AI features unveiled at Config 2024: AI-powered image generation, text rewriting and translation, automatic prototype wiring, and intelligent layer renaming.

The October 2025 acquisition of Weavy, an Israeli AI startup specializing in image and video generation, for over $200 million signaled that Figma's AI ambitions extend well beyond automating repetitive design tasks. Rebranded as Figma Weave and anchored to a new Tel Aviv R&D center, the acquisition brought generative media capabilities into Figma's platform—the ability to create and manipulate images and video using AI, directly within the design environment.

For investors, the AI strategy creates both opportunity and risk. On the opportunity side, AI features that automate the "grunt work" of design—resizing assets, generating variations, translating text, creating placeholder content—make every Figma user more productive and make the platform stickier. On the risk side, AI-powered tools like Google's Stitch (which launched at Google I/O 2025 and received a major update in March 2026) and code-generation platforms like Cursor and Claude Code threaten to bypass the design tool entirely, allowing product managers and developers to generate working interfaces directly from prompts. Figma's gross margin has already declined from ninety-one percent to eighty-three percent over eighteen months, in part due to the infrastructure costs of running AI features. The question is whether AI-driven revenue growth will outpace the margin compression.

VII. Analysis: Porter's Five Forces and Hamilton Helmer's Seven Powers

🎙 The Seven Powers: Where Figma's Moat Is Real and Where It Is Vulnerable

Hamilton Helmer's framework of the Seven Powers—the strategic positions that enable persistent differential returns—provides the most useful lens for evaluating Figma's competitive durability. Three of the seven powers apply clearly to Figma; the others are either absent or contested.

Network Effects are Figma's most visible power. The Figma Community—a marketplace of templates, plugins, design kits, and UI components—creates a classic two-sided network effect. More designers on the platform means more community contributions, which makes the platform more valuable, which attracts more designers. The plugin ecosystem alone numbers in the thousands, with top plugins serving hundreds of thousands of users. Every plugin is a small piece of functionality that a designer would lose if they switched to a competitor. The network effect is not as strong as a social network (designers do not come to Figma to see what other designers are doing the way users come to Instagram to see friends' photos), but it is strong enough to create meaningful friction against churn.

Switching Costs are arguably Figma's strongest power. Enterprise design teams build elaborate component libraries and design systems inside Figma—standardized sets of buttons, icons, typography, color tokens, and layout patterns that ensure visual consistency across an organization's entire product portfolio. These libraries represent thousands of hours of work and are deeply integrated into development workflows. Migrating a mature design system from Figma to a competitor is not a weekend project. It is a multi-month engineering effort with significant risk of breaking downstream code. This is the "System of Record" dynamic: once Figma becomes the authoritative source for an organization's design language, leaving is extraordinarily expensive.

Cornered Resource applies in a specific and underappreciated way. The engineers who know how to build high-performance graphics editors in the browser—the specific combination of WebGL expertise, real-time collaboration infrastructure, and rendering optimization—represent a scarce talent pool that Figma has been accumulating for over a decade. This is not a resource that a well-funded competitor can simply buy off the market. It takes years to develop, and most of the world's experts in this niche already work at Figma.

The powers that Figma does not clearly possess are worth noting. Scale Economies are limited in SaaS businesses generally, and Figma's declining gross margins suggest that scale is not yet translating into cost advantages. Counter-Positioning was a powerful force in Figma's early years—Sketch and Adobe could not respond to browser-native collaboration without cannibalizing their desktop architectures—but it is less relevant now that every competitor has adopted web-based delivery. Branding is strong among designers but has not yet achieved the kind of broad cultural recognition that drives pricing power. Process Power—a persistent organizational advantage in execution—is plausible but hard to evaluate from the outside.

🎙 Porter's Five Forces: The Competitive Landscape in 2026

Threat of New Entrants: High and Rising. This is Figma's most pressing strategic concern. The AI revolution has dramatically lowered the barriers to creating design-like interfaces. Google Stitch, launched in 2025 and updated significantly in March 2026, offers AI-powered "vibe design" capabilities for free, integrated with Google Workspace. The announcement of Stitch's March 2026 update sent Figma's stock down twelve percent in two days. Open-source alternatives like Penpot are gaining traction at a fraction of Figma's price. And the most existential threat may come not from design tools at all, but from AI code-generation platforms that allow non-designers to create functional UIs directly from natural language prompts, potentially rendering the "design file" concept obsolete for certain use cases.

Bargaining Power of Buyers: Low for Enterprise, Moderate for Small Teams. Large enterprises that have built their design systems in Figma have almost no practical ability to switch. The switching costs described above function as a powerful lock-in. For small teams and individual designers, however, the bargaining power is higher—they can experiment with free alternatives like Penpot or Google Stitch without significant migration costs.

Bargaining Power of Suppliers: Low. Figma's primary inputs are cloud computing infrastructure and engineering talent. Cloud costs are competitive and declining. Engineering talent is expensive but not concentrated in a way that gives any supplier pricing power over Figma specifically.

Threat of Substitutes: Moderate to High. The substitutes are not other design tools—they are workflows that eliminate the need for a design tool entirely. If a product manager can describe an interface in words and an AI generates working code, the traditional designer-creates-mockup-developer-implements-it workflow is disrupted. Figma's response—embedding AI deeply into its own platform with products like Figma Make—is an attempt to be the tool through which AI-generated design happens, rather than the tool that AI-generated design replaces.

Competitive Rivalry: Intense. Adobe, despite the failed acquisition and the effective discontinuation of Adobe XD, remains the dominant force in the broader creative tools market and could re-enter the collaborative design space at any time. Canva, valued at $42 billion as of late 2025, competes in adjacent categories and has the brand, the user base, and the capital to push into Figma's territory. Google, with Stitch and the full weight of its AI capabilities, represents the deepest-pocketed potential competitor in the market. And countless AI-native startups are attacking the design workflow from every angle.

Myth vs. Reality: Fact-Checking the Consensus Narratives

Myth: Figma has no real competition. Reality: While Figma holds an estimated eighty to ninety percent share of the UI/UX design market, the boundaries of that market are shifting rapidly. Google Stitch, Canva, and AI code-generation tools are redefining what "design" means, and Figma's share of a narrowly defined market may be less meaningful if the market itself expands or transforms.

Myth: The failed Adobe deal proved Figma is worth $20 billion. Reality: The deal proved that Adobe believed Figma was worth $20 billion to Adobe—a company that would have eliminated its most dangerous competitor and gained a collaboration platform it could not build internally. Figma's standalone value as a public company, measured by the market, sits at roughly $11.5 billion today. The gap between those numbers reflects the difference between strategic value to an acquirer and intrinsic value as an independent entity.

Myth: AI will kill design tools. Reality: AI is more likely to transform design tools than to eliminate them. The need for visual interfaces is not going away. What changes is who creates them and how. Figma's bet—that the right response to AI is to embed it into the design platform rather than cede the workflow to code-generation tools—is reasonable but unproven at scale.

🎙 The KPIs That Matter

For investors tracking Figma's ongoing performance, two metrics stand above all others:

Net Revenue Retention Rate (NRR): This measures how much revenue Figma retains and expands from its existing customer base, excluding new customers. A NRR above 130 percent—meaning existing customers are spending thirty percent more each year—would indicate that Figma's expansion into Dev Mode, FigJam, Slides, and AI features is working. A declining NRR would signal that competitive pressure or pricing pushback is eroding the platform's stickiness.

Number of $100K+ ARR Customers: This metric tracks enterprise penetration—the segment where switching costs are highest, margins are strongest, and competitive moats are deepest. Figma reported 1,119 customers spending over $100,000 annually as of the first half of 2025, up forty-two percent year over year. The trajectory of this number reveals whether Figma is successfully transitioning from a designer-centric tool to an enterprise-wide platform.

VIII. The Playbook: Lessons for the Next Decade

🎙 The Browser-First Mandate

Figma's story encodes a set of strategic lessons that extend far beyond design software, lessons about platform strategy, patience, community, and the courage to bet on technology curves that have not yet arrived.

The first and most fundamental lesson is what might be called the "Browser-First Mandate." In 2012, when Field and Wallace chose to build in the browser, they were not just selecting a delivery mechanism. They were making a philosophical commitment to accessibility, collaboration, and zero-friction distribution. A browser-based tool requires no installation, no updates, no compatibility testing, no IT department approval. It works on a Chromebook in Lagos the same way it works on a MacBook Pro in San Francisco. This architectural choice—made at a time when it was technically painful and commercially unproven—is the reason Figma was able to grow through viral adoption rather than enterprise sales cycles. The lesson for founders: do not build an app if you can build a platform, and do not build a platform on an operating system if you can build it on the web.

The second lesson is community as moat. Figma's plugin ecosystem, its Community marketplace, and its Config conference are not marketing exercises. They are strategic assets that generate network effects, increase switching costs, and outsource R&D to a global community of contributors. When a designer publishes a free UI kit on Figma Community, they are simultaneously creating value for other designers, increasing the platform's attractiveness, and deepening their own investment in the Figma ecosystem. This flywheel is self-reinforcing and extremely difficult for competitors to replicate. Miro has a community. Canva has templates. But neither has achieved the depth of ecosystem integration that Figma has built over a decade of patient cultivation.

The third lesson is perhaps the most counterintuitive: the value of patience in a world obsessed with speed. Figma spent more than three years in stealth building its rendering engine before it had a product. It offered a free tier for years before introducing paid plans. It prioritized user adoption over revenue extraction, knowing that a tool that designers loved and used daily would eventually become a tool that enterprises paid handsomely for. The numbers vindicate this patience. Figma generated $749 million in revenue in 2024 and crossed $1 billion in 2025, with roughly forty percent year-over-year growth even at scale. The company serves ninety-five percent of the Fortune 500 and counts thirteen million monthly active users. From zero revenue to one billion in under a decade—built on a foundation of years of unpaid, unrewarded technical work.

What does Figma become in the next decade? The answer depends on which analogy you prefer. If Figma is "the next Adobe," then it is a creative tools company that will grow into a dominant, profitable platform for professional design, commanding premium prices and high margins. If Figma is "the next Google"—or more precisely, the next Google Docs—then it is something more ambitious: the default collaborative layer through which all digital product development happens, from initial brainstorm to shipped code. The product launches of 2024 and 2025—Slides, Sites, Make, Buzz, Draw, Weave—suggest that Field is aiming for the second vision. Whether the execution matches the ambition is the central question for the next chapter of this story.

The stock market, as of late March 2026, is skeptical. FIG shares sit at roughly $20, down eighty-five percent from the all-time high of $142.92 reached on August 1, 2025, the day after the IPO's euphoric first trading session. The company's market capitalization of approximately $11.5 billion is, in a striking irony, roughly what Adobe was willing to pay in 2022. Gross margins are compressing as AI infrastructure costs rise. Google is giving away a competitive product for free. The AI code-generation movement threatens to disintermediate design tools entirely for certain workflows.

And yet. Figma still grows revenue at forty percent annually. It still serves almost every large technology and consumer company on the planet. Its switching costs for enterprise customers remain formidable. Its founder controls the company and has demonstrated, across fourteen years and multiple crises, the ability to adapt, learn, and build through adversity. The $1 billion breakup fee is spent, but the independence it purchased is paying compound interest in the form of a product portfolio that no competitor can match in breadth or integration.

The story of Figma is, ultimately, the story of a bet—a bet that the browser would become powerful enough to replace the desktop, that collaboration would matter more than features, that patience would beat speed, and that a twenty-year-old college dropout from Sonoma County could build a company that the world's largest creative software monopoly would pay $20 billion to own. The bet on the browser paid off. The bet on collaboration paid off. The bet on patience paid off. Whether the bet on independence—the bet that Figma is better off alone than inside Adobe—will pay off is the question that the market is now pricing in real time, one trading day at a time, under the ticker FIG.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube