Comcast: The Great Separation

I. Introduction & The June 29, 2026 Bombshell

It was 8:26 in the morning, Eastern time, on the last Monday of June 2026, and the tape had not yet opened. Then a single press release crossed the wire and the premarket order book for Comcast Corporation lit up like a switchboard. By the time the opening bell rang on the NASDAQ, the stock — which had spent the better part of three years as one of the most reliably unloved names in large-cap media — was indicated up roughly 22 percent. The reason was a sentence that, a decade earlier, would have been treated as corporate heresy: Comcast intended to break itself in two.[^1]

For the better part of twenty years, the company had preached a single gospel to anyone who would listen. Connectivity and content belonged together. The pipes carried the shows; the shows filled the pipes; the theme parks turned the shows into pilgrimages; and the whole thing spun faster and faster in a virtuous loop that management never tired of calling the "flywheel." Brian Roberts, the soft-spoken chairman who had inherited the throne from his father, had bet the company on that thesis — first by swallowing a cable rival twice his size, then by buying a Hollywood studio and a broadcast network, then by paying a king's ransom for a European satellite empire. The argument was always the same: scale plus integration equals an unassailable moat.

And now, on a Monday morning, that argument was being quietly euthanized. The release announced that Comcast would separate into two independent, publicly traded companies. On one side: a pure-play connectivity and infrastructure business — broadband, wireless, and the highly profitable Comcast Business franchise — to be run by Michael Angelakis, the disciplined former chief financial officer who had been summoned back from the world of private capital to take the helm. On the other: a premium entertainment company built from the bones of NBCUniversal and Sky — Universal Pictures, the NBC and Telemundo broadcast networks, the Peacock streaming service, and the theme-park empire anchored by the brand-new Epic Universe in Orlando — to be led by Mike Cavanagh, the former JPMorgan banker who had risen to co-chief executive.[^1]

The market's euphoric reaction deserves a moment of skepticism, because the cheering crowd was not celebrating a triumph. It was celebrating an admission. Wall Street had spent years applying what it calls a "conglomerate discount" to Comcast — valuing the sum of the company's parts at less than what each piece might fetch on its own — precisely because investors no longer believed the flywheel story. The Wall Street Journal, in a piece published that same morning under the headline "The Death of the Telecom-Media Conglomerate," framed the split as the formal end of an era that had begun with the AOL–Time Warner merger a quarter-century earlier and was now ending in a wave of corporate divorces.1 A 22 percent pop is not the sound of a strategy vindicated. It is the sound of a discount being released.

So what actually happened here? How did a company that built one of the most aggressive acquisition machines in American corporate history — a machine that, at its peak, controlled a roughly $150 billion media-and-telecom empire — arrive at the conclusion that its own integration was the problem? And what does the architecture of this separation tell us about who really controls Comcast, and on whose behalf?

This is the story we want to tell. It runs from a 1,200-subscriber cable system in Tupelo, Mississippi, to the ultimate vertically integrated media conglomerate, and finally to the great unwinding. Along the way we will dissect the capital-allocation report card — the masterclass that was NBCUniversal, the disaster that was Sky — and the brutal, changing economics of selling internet access in an age when your customers suddenly have alternatives. And we will spend real time on the strangest fact of all: the governance machinery that let one man, holding well under one percent of the economics, steer this entire ship. Because to understand the separation, you first have to understand the fortress.

II. The Super-Voting Fortress & Family Control

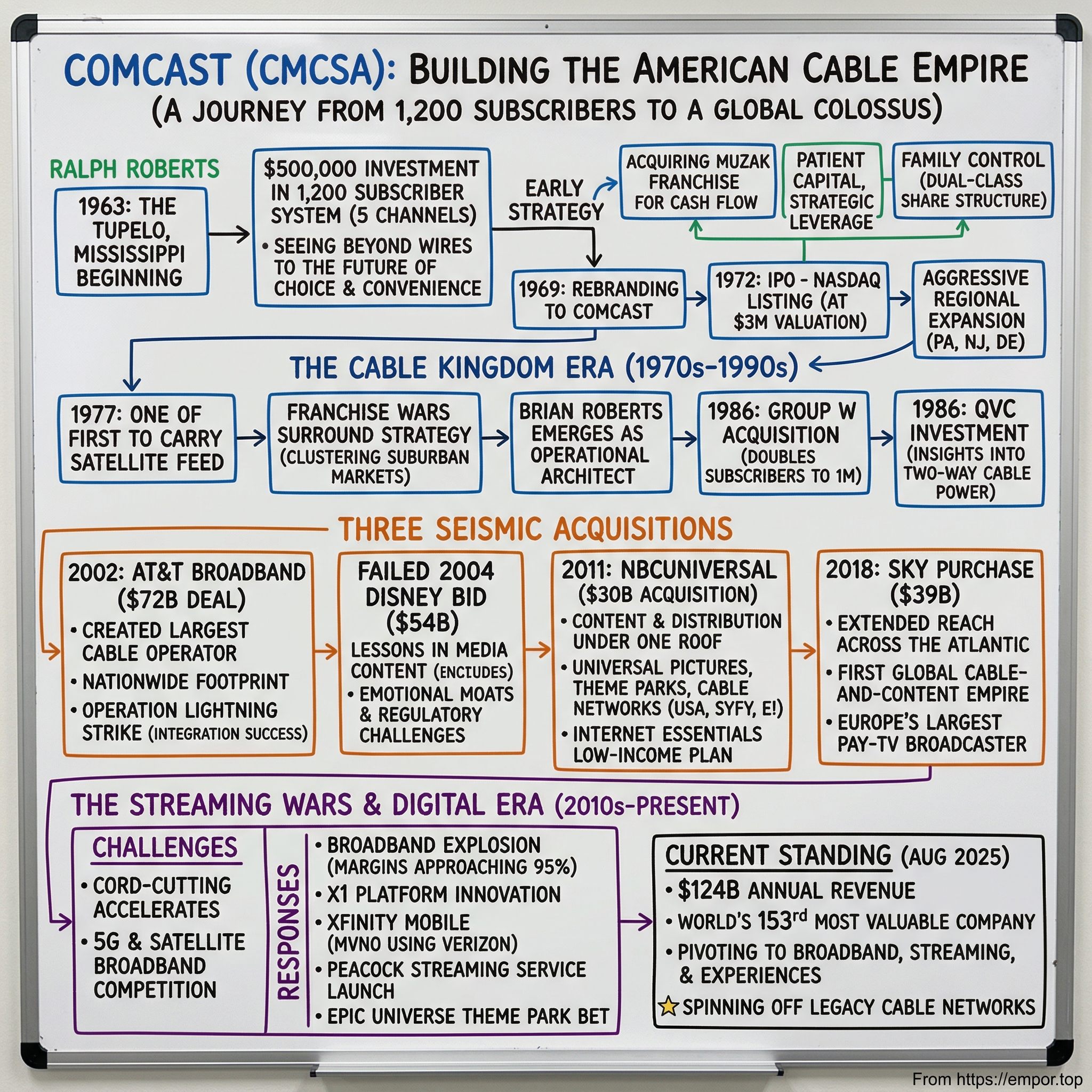

Picture Tupelo, Mississippi, in 1963 — Elvis Presley's hometown, a modest county seat in the northeast corner of the state. A belt manufacturer from Philadelphia named Ralph Roberts, who had recently sold his company and was looking for his next act, traveled down and bought a small cable television system serving roughly 1,200 subscribers. In that era, "cable" was not the entertainment colossus it would become; it was a humble utility called CATV — community antenna television — that existed for one prosaic reason. People in hilly or remote places could not pull a clean broadcast signal out of the air, so an operator would erect one good antenna on a hilltop, capture the signal, and pipe it into homes by wire for a monthly fee. That was the entire business. Ralph Roberts saw something the sellers did not: a subscription utility with a captive footprint.

It is worth pausing on the economics of that early cable system, because they are the genetic code of everything Comcast became. Building a cable plant is brutally capital-intensive up front — you have to string wire down every street, past every home, whether or not anyone subscribes. But once the plant is built, the cost of adding one more customer, or of delivering one more channel to an existing customer, is close to nothing. That combination — enormous fixed cost, near-zero marginal cost — produces ferocious operating leverage. Every incremental subscriber after you cross breakeven drops almost straight to cash flow. It also produces a natural local monopoly, because no rational competitor wants to build a second set of wires down a street that already has one. For decades, that was the quiet magic of cable: a regulated-utility cost structure with the pricing freedom of a monopoly. Hold that thought, because the central drama of this entire story is what happens when the monopoly stops being a monopoly.

The company Ralph built methodically — renamed Comcast, a contraction of "communications" and "broadcast" — passed in 2002 to his son. Brian Roberts had grown up inside the business, and when he formally took over as chief executive he inherited not just a company but a philosophy of control. The Roberts family did not intend to build an empire only to have it taken from them by a hostile bidder or wrestled away by activist investors. So they engineered something extraordinary, and it is the single most important structural fact about Comcast that most casual observers never grasp.

Brian Roberts personally owns essentially all of Comcast's Class B common stock — roughly 9.4 million shares — a tiny sliver of a company with billions of shares outstanding.3 But those Class B shares are not ordinary. By the terms of the charter, the Class B stock carries a fixed, non-dilutable 33⅓ percent of Comcast's total voting power. Read that again: no matter how many new shares the company issues to make acquisitions, no matter how the public float grows, Roberts's block of votes cannot be diluted below one-third of the total.3 And here is the punchline that makes the arrangement so remarkable — his economic stake in the company, the actual claim on its profits and assets, sits well below one percent.

Let us translate that out of the language of securities law. Brian Roberts controls, by an iron mathematical guarantee, the largest single voting bloc in a company in which he owns almost none of the money. One-third of the votes is, in practice, a veto over anything that matters: no merger, no board overhaul, no charter change, no activist campaign can succeed without him. This is the "voting fortress," and it has had two faces throughout Comcast's history. The flattering face is that it gave management the freedom to act boldly and play long — to make enormous, contrarian, multi-decade bets without flinching at quarterly noise or fending off raiders. It is hard to imagine a quarterly-driven, takeover-exposed company ever committing the capital that built Xfinity or bought NBCUniversal.

The unflattering face is the one a neutral investor has to weigh just as seriously. A 33⅓ percent voting lock with a sub-1 percent economic stake means the public shareholders who supply nearly all of the capital have almost no mechanism to hold the controlling shareholder accountable. If management destroys value — and we will see at least one episode where it did, spectacularly — there is no realistic path for outside owners to force change. There is no activist who can win a proxy fight against a one-third bloc. There is no acquirer who can go hostile. The accountability that ordinarily disciplines public companies simply does not apply here. That is not a moral judgment; it is a structural fact, and it is the lens through which every decision in this story should be read.

Which brings us to the most telling detail of the June 2026 separation. When you split a company, you have to decide how the new entity will be governed — and Comcast chose to clone the fortress. The separation is being structured so that the same dual-class architecture carries over: Brian Roberts is set to hold the identical non-dilutable 33⅓ percent voting control of both the connectivity company and the media company.[^1] He is not loosening his grip as part of this divorce. He is duplicating it. One controlling shareholder, two empires, the same veto in each. Whatever else the separation unlocks for public shareholders, governance reform is not on the menu. And that tension — between the value the split might release and the control it leaves untouched — is the through-line of everything that follows, starting with the acquisitions that built the empire in the first place.

III. The M&A Playbook: Masterclass vs. Disaster Class

If you want to understand a company that grew chiefly by acquisition, do not read the press releases. Read the price tags, and then read what each asset was worth a decade later. By that unforgiving standard, Comcast's dealmaking record is not one story but three: a foundational land-grab, a genuine masterclass, and a textbook disaster. Together they form one of the more instructive capital-allocation case studies in modern American business, precisely because the same management team, operating under the same governance, produced all three.

Start with the land-grab. In December 2001, Comcast won a hard-fought auction for AT&T Broadband — the sprawling cable arm that the telephone giant had assembled and then decided to shed — and the deal closed in November 2002 in a transaction valued at roughly $72 billion.4 To grasp the audacity here, you have to understand the relative sizes. Comcast was swallowing an operation larger than itself. The combined company emerged with something on the order of 22 million subscribers, nearly twice the size of the next-largest cable operator in the country, with wires running into roughly one in five American homes.4 In a single stroke, Comcast went from being one large regional cable operator to being the national cable platform. This is the deal that drew the map. The footprint that consumers know today as Xfinity — the physical cable plant passing tens of millions of homes — is, in large part, the AT&T Broadband footprint rebranded and upgraded. Without it, there is no broadband cash machine to speak of, because there are no wires.

The land-grab gave Comcast its pipes. The masterclass gave it content — and it is worth slowing down to admire the financial engineering, because this is the deal Comcast bulls point to when they argue that the company can, in fact, allocate capital brilliantly. In 2011, Comcast did not simply buy NBCUniversal outright. It bought a 51 percent controlling stake from General Electric, and it structured the purchase cleverly: rather than paying all cash, Comcast contributed its own portfolio of cable channels plus cash into a joint venture, so the effective check it wrote was far smaller than the headline enterprise value. Two years later, in February 2013, with NBCUniversal's cash flows visibly improving in its hands, Comcast moved early to buy out GE's remaining 49 percent for approximately $16.7 billion, taking the asset to 100 percent ownership.[^7]5

Here is why this was a masterclass and not merely a large deal. The valuation Comcast paid implied a total enterprise value for NBCUniversal in the low-to-mid thirty-billion-dollar range — a strikingly modest price for a collection of assets that included a major film studio, a broadcast network, a stable of cable channels, and, crucially, a theme-park business with enormous latent value. GE, an industrial conglomerate that viewed media as a non-core orphan, was a motivated seller; Comcast was a patient, knowledgeable buyer who understood exactly what the cash flows could become. And then Comcast did the thing that separates good acquirers from lucky ones: it reinvested. Traditional, sticky cable cash flows were funneled into reviving Universal Pictures' film slate and, above all, into a massive expansion of the high-margin theme-park segment. The parks, almost an afterthought in the original deal math, would grow into one of the crown jewels of the entire company. Buy a great asset cheap from a disinterested seller, then pour capital into its best segment — that is the playbook, executed nearly flawlessly.

And then came Sky, the disaster, where the very same instincts that made the NBCUniversal deal a triumph curdled into hubris. By 2018, Comcast had decided that its future required a major international footprint, and the prize it fixed on was Sky — the dominant pay-television operator across the United Kingdom, Ireland, Italy, and Germany, with tens of millions of subscribers and a respected original-content operation. The problem was that Disney, in the course of acquiring most of Twenty-First Century Fox, was also pursuing Sky. What followed was extraordinary: British regulators ordered the contest settled by a rare, three-round sealed-bid auction conducted over a single September weekend in 2018.6

Imagine the scene. Two of the largest media companies on earth, forbidden from negotiating, each submitting blind bids with no knowledge of what the other had written down — pure auction theory, played for tens of billions of dollars. When the envelopes were opened, Comcast had won with a bid of £17.28 per share, a figure that valued Sky at roughly £30.6 billion, or about $39 billion.6 Comcast had beaten Disney. But "winning" a blind auction has a darker name in finance: the winner's curse. The party that prevails in a sealed-bid contest is, by definition, the one who was willing to pay the most — which often means the one who overestimated the asset by the widest margin. Comcast's winning price represented a substantial premium over where Sky had historically traded and over comparable pay-TV multiples.

The aftermath validated the skeptics. Sky's core proposition rested on the premium economics of satellite pay-television distribution — and almost immediately, the ground shifted beneath it. European cord-cutting accelerated. The streaming wars arrived in Europe just as they had in America. The premium that satellite distribution had long commanded began to evaporate as global streamers reached consumers directly. An asset bought at the top of the pay-TV cycle saw its competitive position erode, and Comcast was eventually forced into multibillion-dollar goodwill impairments tied to Sky — the accounting system's blunt way of admitting that the company had paid for value that no longer existed. As a study in capital allocation, Sky is the mirror image of NBCUniversal: instead of buying a great asset cheap from a tired seller and harvesting it, Comcast paid a peak price for a structurally challenged asset in a competitive frenzy, and then watched the structural challenge consume the premium. It is the single clearest example in the company's history of what the controlling-shareholder structure permits — a bold, irreversible bet with no external mechanism to stop it — turning against the public owners who funded it.

The final chapter of the M&A story is the deal that did not happen, and it matters because it helped trigger everything else. As the media industry consolidated into the mid-2020s, Comcast was widely reported to have explored a combination with Warner Bros. Discovery — a logical move to add scale to its content arm. That pursuit ultimately came to nothing; the Warner assets moved in a different direction, toward a Paramount-led tie-up, leaving Comcast's media division without the consolidating partner it had sought. The failure was clarifying. If you cannot get bigger in content, and content is dragging down the multiple the market assigns to your pipes, then perhaps the answer is not to get bigger at all. Perhaps the answer is to get smaller — to separate. The missed Warner deal helped push Comcast off the acquisition treadmill it had ridden for two decades and toward the unwinding. But before we get to the unwinding, we have to understand the asset that was always the real prize: the cash machine in the wires.

IV. The Cash Machine: Connectivity, Platforms & The Broadband Battleground

Strip away the movie premieres and the roller coasters and the red-carpet glamour, and look at where Comcast's money actually comes from, and you arrive at an unglamorous truth that the entertainment headlines have spent years obscuring. The Connectivity & Platforms segment — broadband, wireless, business services, the wires and the bytes — generated the majority of the company's revenue, on the order of 57 percent, and an even more dominant share of its consolidated cash flow.[^3]2 This is the gravity well of the entire enterprise. Whatever multiple Wall Street assigns to Comcast, it is ultimately assigning it to the durability of these connections. The terminal value of this company lives in the pipes, not on the screen.

For most of Comcast's modern history, this was the easiest money in American business. Residential broadband was a quasi-monopoly with a wonderful growth algorithm: every year you added subscribers as more of life moved online, and you raised prices, and your marginal cost of serving each new customer was trivial. Add units, raise prices, print cash. But around the mid-2020s, the first half of that algorithm broke, and the entire investment thesis for the connectivity business shifted from a growth story to something far more contested.

The clearest evidence sits in a single, sobering data point. In the first quarter of 2026, Comcast reported that its domestic broadband subscriber base actually shrank — a net loss of roughly 65,000 customers in the quarter.[^3] For a business whose entire historical identity was built on relentless net additions, a negative number is not a rounding error; it is a regime change. The company that could once count on adding subscribers every single quarter could no longer do so. And the reason is the most important competitive development in this story: for the first time in the history of cable, the customer has real alternatives. The local monopoly we described back in Tupelo has been broken on three separate fronts at once.

The first front is fixed wireless access, or FWA, and it is the one that has done the most immediate damage. The idea is deceptively simple. The big mobile carriers — T-Mobile and Verizon — have spent fortunes building out 5G networks, and they discovered they had spare capacity. So they began selling home internet that arrives not through a wire in the ground but over the air, through the same cellular towers that serve phones. The customer plugs in a small box, and broadband appears — no installation crew, no buried cable, often at a flat price that undercuts cable by a wide margin. For a household that mostly streams video and browses, FWA is, functionally, good enough. It has been especially lethal at the lower end of Comcast's customer base — the price-sensitive subscribers for whom "good enough and cheaper" is an easy trade. FWA did not have to be better than cable to hurt cable. It only had to be adequate and inexpensive, and it is both.

The second front is fiber-to-the-home, and it is the one that threatens the high end. Here the attackers are the telephone companies — AT&T and Verizon chief among them — overbuilding Comcast's cable plant with fiber-optic lines run all the way to the house. The technical distinction matters, so let us make it plain. Comcast's network is a hybrid: fiber for the long-haul backbone, but coaxial copper cable for the final stretch into homes — the legacy of that AT&T Broadband footprint. Copper coax is excellent at delivering fast download speeds but has historically been far weaker at uploads, producing the lopsided "asymmetrical" connections most cable customers have always lived with. Pure fiber, by contrast, offers symmetrical speeds — as fast up as down — which matters increasingly in a world of video calls, cloud backups, gaming, and remote work. When a fiber overbuilder shows up on a street, it offers a genuinely superior product, and it tends to peel away exactly the affluent, high-usage households that are Comcast's most valuable customers.

The third front is the one that lives in the sky and the imagination, and it is the longest-dated threat: satellite broadband, embodied by Elon Musk's Starlink. By beaming connectivity directly from a constellation of low-orbit satellites, Starlink can reach places no wire ever will, and investor enthusiasm around it has only intensified following the SpaceX initial public offering, which gave the market a fresh, eye-watering valuation to anchor on. For now, Starlink is most threatening at the rural fringe rather than in the dense suburbs where Comcast makes its money. But it is a robust, improving substitute that did not meaningfully exist a few years ago, and a neutral observer has to file it under "structural, long-term, and not going away."

Faced with this three-front war, how is management responding? The official answer is a generational network upgrade. Comcast is rolling out a new cable standard called DOCSIS 4.0, and the technology deserves a plain-English explanation because management leans on it heavily. DOCSIS 4.0 is essentially a way to wring symmetrical, multi-gigabit speeds out of the existing coaxial cable already buried in the ground — closing the upload gap with fiber without having to dig up every street and lay new glass. If it works as advertised, it lets Comcast match fiber's headline capabilities at a fraction of fiber's construction cost and time. That is the bull case for the network, and it is not trivial: re-using the installed plant is a real cost advantage over an overbuilder starting from scratch.

But upgrades are not free, and here we arrive at the number that is squeezing the connectivity story in the near term. Comcast has designated 2026 as its peak year for capital expenditure — the heaviest spending year of the DOCSIS 4.0 build-out — which weighs directly on margins and free cash flow precisely when the subscriber base is under attack.[^3]2 The neutral framing is uncomfortable for management: the company is being forced to spend the most to defend its network at the very moment its pricing power is being most visibly challenged. That is the opposite of the old algorithm. Investors are now being asked to fund a defensive capital cycle and trust that pricing — raising average revenue per user, or ARPU, on existing customers — can offset the loss of units. Whether pricing power survives contact with three sets of cheaper, faster, or more flexible competitors is the central open question of the entire connectivity thesis, and the Q1 2026 subscriber loss is the first hard evidence that the answer is "not entirely."[^3]

It would be a mistake, though, to reduce Connectivity & Platforms to embattled residential broadband, because two segments inside it are doing genuinely well and are large enough to move the needle. The first is Comcast Business — the franchise that sells connectivity and managed services to enterprises, from corner stores to large corporate accounts. This is a multibillion-dollar revenue engine, comfortably north of $10 billion, growing at mid-single-digit rates, and carrying EBITDA margins above 55 percent.2 Those are extraordinary economics, and they are far more defensible than the consumer business because switching providers is a painful, disruptive decision for a company that runs its operations over those connections. Comcast Business is, in many ways, the quiet crown jewel of the connectivity company — a large, growing, high-margin asset that the entertainment drama has long overshadowed.

The second standout is Xfinity Mobile, and its strategic logic is more important than its raw size. By the end of 2025 Comcast had built its wireless line count past 9 million, adding roughly 1.5 million lines in 2025 alone.[^3]2 What makes this clever is how Comcast offers wireless without owning a wireless network. It operates as a mobile virtual network operator, or MVNO, riding on Verizon's network under a wholesale agreement — meaning Comcast sells mobile service while sidestepping the staggering capital cost of building cell towers. The point of Xfinity Mobile is not really to make a fortune in wireless; it is to defend broadband. A household that buys both internet and mobile from Comcast, bundled together on one bill, is markedly less likely to churn away to a competitor. In a world where FWA and fiber are prying customers loose, the bundle is the glue, and wireless is the cheapest, most capital-light glue Comcast has. The irony is delicious and worth noting: Comcast defends itself against Verizon's fiber and FWA by renting Verizon's own wireless network to lock in its broadband base.

So what should an investor take from all this? The connectivity business remains a formidable cash generator with two genuinely strong franchises in business services and the wireless bundle. But the core consumer broadband moat — the local monopoly that was the foundation of the entire company — has demonstrably cracked. The evidence is not rhetorical; it is in the negative net adds and the peak-capex cycle. The question is no longer whether Comcast's pipes make money, but whether they can keep raising prices as the monopoly becomes a competitive market. That uncertainty about the cash machine is exactly what made the other half of the company — the volatile, capital-hungry media business — feel like a liability worth shedding.

V. The Media Spin Cycle: From Synergy to Separation

For most of the twentieth century, the economics of television were a license to print money, and the machine that printed it was something called the carriage fee. A cable network like USA or CNBC would charge every cable operator a few dollars per subscriber per month, whether or not anyone actually watched, and on top of that it sold advertising against the audience it did attract. Dual revenue streams, enormous margins, and — because the cable bundle was effectively compulsory — almost no churn. It was, in its way, the content equivalent of the broadband monopoly: a toll booth on an essential utility. And then streaming detonated the whole arrangement.

The brutal arithmetic of the streaming transition is the single most important thing to understand about why the media business became a problem rather than a prize. In the old linear world, a media company collected guaranteed carriage fees from roughly 100 million cable households, most of whom never watched its channels but paid anyway. In the new direct-to-consumer world, that same media company has to persuade each household, one at a time, to actively choose and pay for its app — and the revenue per subscriber is lower, the churn is higher, and the cost of the programming required to attract and retain those subscribers is enormous and front-loaded. Companies across the industry essentially traded a large, high-margin, declining business for a smaller, low-margin, growing one, and called it progress. For years, the streaming wars destroyed industry profitability because everyone was spending to win subscribers in a market where the unit economics simply did not support the spending.

Comcast's entry in that war is Peacock, and its results capture the trap perfectly. By the first quarter of 2026, Peacock had pushed past 46 million paid subscribers and generated roughly $2.1 billion in quarterly revenue — genuinely impressive scale, achieved faster than skeptics expected.[^3] And yet Peacock remained a money-losing operation, still in an EBITDA-loss phase, because the cost of the programming required to attract those subscribers — live sports, films, originals — ran ahead of the revenue they brought in.[^3] This is the streaming paradox in miniature: the service can be growing and successful by every subscriber metric and still be a drag on profits, because each new subscriber arrives attached to a content bill. A neutral reading is that Peacock has proven it can attract an audience but has not yet proven it can do so profitably — and "not yet" is doing a great deal of work in that sentence.

Faced with a content portfolio that mixed structurally declining linear channels with structurally unprofitable streaming, Comcast made its move in two acts. The first act came in January 2026, and it was the warm-up for everything that followed. Comcast spun off the bulk of its traditional cable networks — CNBC, MSNBC (rebranded, in a detail that captures the era's strangeness, as "MS NOW"), USA Network, E!, Syfy, Oxygen, and Golf Channel, among others — into a separate, independent company called Versant Media Group, which completed its separation and began trading at the start of 2026.7 Versant was handed to Mark Lazarus, a veteran NBCUniversal executive named its chief executive in late 2025.[^11]

The strategic logic of the Versant spinoff was clarifying, and it told you exactly how management had come to see these assets. These were the channels facing the most relentless structural decline — the toll booths on a road that fewer and fewer cars were taking, as cord-cutting drained the linear bundle year after year. By packaging them off into a separate vehicle, Comcast accomplished two things at once. It removed a shrinking, low-multiple business from its own reported results, instantly improving the parent's growth and margin profile on paper. And it gave those channels their own management, free to run them for cash and consolidation rather than as neglected stepchildren inside a giant. The unspoken message was unmistakable: Comcast had decided that linear cable networks were not assets to nurture but assets to exit. For a company that had paid billions to acquire many of those very channels, that was a remarkable reversal — and it was only the appetizer.

The main course is the separation announced this very morning: the spinoff of the rest of NBCUniversal and Sky — Universal Pictures, the NBC and Telemundo broadcast networks, Peacock, the Sky operations, and the theme parks — into a standalone entertainment company under Mike Cavanagh.[^1] And to understand why the timing landed in mid-2026, you have to understand a roller coaster.

In May 2025, Comcast opened Epic Universe, a sprawling new theme park in Orlando — the first entirely new major theme park built in that market in a generation, anchored by elaborately themed lands including a Super Nintendo World built in partnership with 任天堂 Nintendo.10 Epic Universe was not just another attraction; it was a step-change in the scale and earnings power of the experiences business. Theme parks are, in capital-allocation terms, the most attractive asset in the entire media portfolio: they own irreplaceable physical locations and beloved intellectual property, they command pricing power that streaming can only dream of, and once built, a successful park throws off cash for decades. The opening of Epic Universe gave a powerful lift to experiences earnings, and — crucially for the separation thesis — it made the parks-and-studios entertainment company strong enough, and profitable enough, to stand on its own two feet.10 You cannot spin off a business that the market will treat as a basket of losses; Epic Universe helped ensure that the media company would walk out the door with a genuine growth engine, not just Peacock's red ink and Sky's faded glory.

Which brings us to the financial concept that the entire separation is built to exploit: the conglomerate discount. Wall Street has a well-documented habit of valuing diversified companies at less than the sum of their parts, and the logic is straightforward. A pure-play broadband-and-wireless investor wants stable, utility-like cash flows and dividends, and is repelled by the volatility and capital intensity of a Hollywood studio. A pure-play media investor wants exposure to hit films and growing parks, and is bored by the slow grind of a connectivity utility. Forced to own both in a single stock, each type of investor applies a discount for the half they did not want — and the blended multiple sags. The separation's central financial bet is that by cleaving the company in two, each piece will attract its natural shareholder base and command a higher multiple, so that two focused companies are worth more than one sprawling conglomerate. That is the theory the 22 percent premarket pop was pricing in.1

A neutral investor, though, should hold two thoughts at once. The conglomerate-discount logic is real and well-supported by decades of corporate-finance evidence; splits like this often do release trapped value. But it is also worth noting what the split does not fix. It does not make broadband's competitive problem go away, and it does not make streaming profitable. It rearranges the deck so that each problem is now visible in isolation, owned by investors who signed up for exactly that risk. Separation is a financial and governance maneuver, not an operating cure. Which makes the question of who runs each company, and how they are paid to run it — the human and incentive architecture of the split — the next thing we have to examine closely.

VI. Management, Incentives & Governance Analysis

Every corporate separation is, at bottom, a story about people and the incentives you build around them — because the moment you cut a company in two, you have to decide who gets the wheel of each new vehicle, and how richly they are rewarded for where they steer it. Comcast's answer to that question is revealing, both for who was chosen and for how their pay is structured.

Take the media company first, because its chosen leader is the more telling appointment. Mike Cavanagh, who turned 60 around the time of the separation, did not come up through Hollywood. He came up through Wall Street — a former chief financial officer of JPMorgan Chase, a numbers man and a banker, who joined Comcast and rose to become co-chief executive before being tapped to run the spun-off NBCUniversal and Sky.[^1] That a financier rather than a creative was handed the keys to a studio-and-parks empire tells you something about how Comcast views the assignment: this is a capital-allocation and value-realization job at least as much as it is a content job. Cavanagh's task is not primarily to green-light the next blockbuster; it is to maximize the equity value of a newly independent entertainment company in a hostile media market — to make the conglomerate-discount thesis actually pay off.

And he is being paid, lavishly, to do precisely that. Cavanagh's total compensation for 2025 came to a staggering $71.8 million, a figure that places him among the most richly rewarded executives in American media.8 The headline number, though, is less interesting than its structure. As part of his elevation, Comcast granted Cavanagh a $35 million performance stock unit award — a special promotion grant designed to cliff-vest in 2029, contingent on hitting rigorous performance targets.8 The phrase "cliff-vest" matters: it means he receives nothing from that grant unless he is still there and the targets are met when the cliff arrives. Translated into plain incentive language, the arrangement bolts Cavanagh to the windshield of the media company for the next several years and ties an enormous slice of his personal wealth to the equity value he can create in the spun-off entity. From an alignment standpoint, that is exactly what a shareholder in the new media company would want — a leader whose payday depends on the stock he is being asked to build. From a skeptic's standpoint, it is also a reminder that the people designing these separations stand to capture extraordinary sums if the financial engineering works.

The connectivity company's chosen leader tells a different and, in some ways, more surprising story. Michael Angelakis, 62, is not a new face at Comcast at all — he is a returning one. Angelakis served as the company's chief financial officer from 2007 to 2015, the very years that spanned the original NBCUniversal acquisition, and he was deeply involved in the financial architecture of that masterclass deal. After leaving the CFO chair, he ran a Comcast-backed investment vehicle, operating in the world of private capital and earning a reputation as a disciplined, returns-focused allocator. Now he has been summoned back to run the remaining Comcast — the broadband-and-wireless utility.[^1] The symbolism is hard to miss: the man who helped engineer Comcast's most celebrated acquisition is being brought back to preside over the dismantling of the empire that acquisition helped build. For a connectivity business entering a defensive capital cycle against three sets of competitors, a hard-nosed capital allocator is a logical choice. The question a neutral observer should ask is whether disciplined allocation is enough when the underlying product is losing its monopoly — discipline can optimize a declining business, but it cannot, by itself, reverse a structural decline.

Now for the part of this section that a genuinely independent analysis cannot skip: management credibility. And here the record contains a pattern worth naming plainly. For more than a decade, Comcast's leadership told investors a specific and confident story — that the combination of connectivity and content was a unique competitive advantage, a flywheel that rivals could not replicate, the strategic logic that justified buying NBCUniversal and paying up for Sky. The flywheel was not a passing talking point; it was the central organizing narrative of the company, repeated across years of earnings calls and investor presentations. And then, in the span of roughly six months across late 2025 and the first half of 2026, that narrative was simply abandoned — first with the Versant spinoff, then with today's far larger separation — without a clear, candid explanation of why the flywheel that had justified twenty years of acquisitions had suddenly stopped working.[^1]7

That is the kind of unexplained strategic reversal that an investor is entitled to treat as an analytical fact, not a footnote. When management spends a decade insisting that integration is the moat and then dismantles the integration in two rapid moves, one of two things must be true: either the original thesis was wrong, or the new one is. Comcast has not really told its owners which. A management team that changes its central strategic narrative this sharply, this fast, has — at minimum — spent some of its credibility, and the burden now sits with results to rebuild it.

The credibility question extends to how management has explained the broadband troubles. The official framing has leaned on macroeconomic softness and the rise of fixed wireless competition as the causes of subscriber losses.[^3] Both are real factors. But a neutral reading notes what tends to get less emphasis: the slower upgrade cycle of Comcast's hybrid fiber-coax network relative to pure fiber, which is partly a function of choices the company itself made about how aggressively to invest over the prior decade. Attributing losses primarily to external forces — the economy, the competitors — while underplaying the internal, structural elements is a familiar pattern in corporate communication, and it is worth watching whether management's explanations grow more candid as the DOCSIS 4.0 cycle plays out.

To be fair to the other side of the ledger, the capital-allocation record is not all Sky. Comcast has been a serious returner of cash, generating substantial free cash flow — on the order of $19 billion in 2025 — and deploying it across a steady, growing dividend and large share repurchases.[^3]2 A company that throws off that kind of cash and returns much of it has earned some benefit of the doubt on shareholder friendliness. The honest scorecard reads something like this: a genuinely strong cash-generation and capital-return engine, a masterclass acquisition early, a value-destroying overpayment in the middle, and a strategic narrative that has just been reversed without full explanation — all under a governance structure where the public owners who funded every bit of it have no real means to influence any of it. That combination is exactly why the next question — how to weigh the powers and forces arrayed around each new company — has to be answered without taking management's word for the outcome.

VII. Strategic Frameworks: 7 Powers & Porter's 5 Forces

To judge whether the two companies emerging from this separation can actually defend their profits, it helps to move from narrative to framework — to ask, in the structured language of competitive strategy, what durable advantages each business really possesses, and what forces are pressing against them. Two lenses are useful here: Hamilton Helmer's 7 Powers, which catalogs the genuine sources of sustained competitive advantage, and Michael Porter's Five Forces, which maps the structural pressures of an industry. Let us run both companies through them, with a neutral eye.

Begin with the connectivity company and Helmer's framework. The clearest power it holds is scale economies, and they are formidable. The physical cable plant — the network passing tens of millions of homes, built and accumulated over decades and at the cost of tens of billions of dollars — is something no new entrant can casually replicate. The high fixed cost of the network is spread across an enormous subscriber base, giving Comcast a lower cost per customer than any sub-scale competitor could achieve. And the DOCSIS 4.0 upgrade reinforces this power: the ability to wring fiber-class speeds out of already-buried coaxial cable is a cost advantage rooted directly in the scale of the installed plant. A fiber overbuilder has to dig up the street; Comcast, in theory, just upgrades the electronics. That is scale economics doing real work.

The second power the connectivity business holds is switching costs, though here we should be more measured. There is genuine friction in changing internet providers — the hassle of scheduling an installation, of migrating email addresses, of reconfiguring smart-home devices and saved networks, of the simple inertia that keeps households with the provider they have. The Xfinity Mobile bundle deliberately deepens that friction: a customer with internet and wireless on one bill faces a bigger, more annoying decision to leave. But switching costs in broadband are only moderate, not high, and the evidence proves it — the negative net adds of early 2026 show that when a cheaper or better alternative appears on the street, a meaningful number of customers will, in fact, overcome the friction and leave.[^3] Switching costs slow the bleeding; they do not stop it.

Now the media company, where the powers are different and, in one respect, stronger. The standout is cornered resource — Helmer's term for preferential access to a coveted asset that others cannot obtain on equal terms. The spun-off NBCUniversal owns exactly this: elite, irreplaceable intellectual property. The animation franchises of Illumination (think the Minions) and DreamWorks, the Universal film library, the characters that populate the theme parks — these cannot be recreated by a competitor with a checkbook. Layered on top is preferential access to premium live sports rights, including NBC's major multi-billion-dollar NBA package commencing with the 2025–26 season, alongside its long-standing NFL and Olympics relationships. Live sports is the last reliably appointment-viewing content in a fragmented world, and the rights are genuinely scarce. The media company also enjoys real scale economies of its own — in global film production and distribution infrastructure, where the fixed cost of a studio and a worldwide distribution network is spread across a large slate.

A neutral caveat belongs here, though: a cornered resource is only as valuable as the economics of the window you exploit it through. Owning the NBA rights is a power; paying for them in an era when linear advertising is shrinking and streaming has not yet proven profitable is a cost. The same IP that anchors a wildly profitable theme park also anchors a money-losing streaming service. The power is real; whether it is monetized at an attractive return depends on execution in a hostile market.

Now turn Porter's Five Forces on the connectivity company, since that is where the company's terminal value sits and where the competitive picture has changed most dramatically. The threat of new entrants is low — and this remains the connectivity business's single best structural feature. The capital cost of building a physical network to pass millions of homes is so staggering that no one is going to spin up a brand-new wireline competitor from scratch. That barrier is as high as ever.

But the other forces have all moved against Comcast. The bargaining power of buyers is now moderate-to-high, a genuine break from history. For the first time, ordinary consumers have realistic alternatives — fixed wireless and fiber overbuilders — which means they can negotiate, threaten to leave, and act on the threat. A customer with options has power; a customer in a monopoly has none, and Comcast's customers are no longer in a monopoly. The threat of substitutes is high, and this is the crux: fixed wireless access and satellite services like Starlink are not merely theoretical alternatives but functioning substitutes that are already taking subscribers, particularly at the price-sensitive low end and the rural fringe. The bargaining power of suppliers is low-to-moderate — Comcast is a large enough buyer of network equipment to command good terms, but it is worth noting a specific dependency: its Xfinity Mobile bundle, the very tool it uses to defend broadband, rides on Verizon's network under a wholesale MVNO agreement, which gives a direct competitor a degree of leverage over a key piece of Comcast's retention strategy. And finally, competitive rivalry is high — a genuine three-way war among cable, telco fiber, and wireless FWA, each attacking from a different technological direction.

The rivalry deserves one extra beat, because it is intensifying through consolidation. In 2026, two of Comcast's largest cable peers — Charter Communications, with roughly 30 million broadband subscribers, and Cox Communications — moved to combine in a megamerger, filing their regulatory application with the FCC in May.9 The logic is defensive: in a market where scale is the chief weapon and the monopoly era is over, the surviving cable operators are bulking up to spread their own fixed costs and network-upgrade burdens across an even larger base. Comcast is not the only incumbent feeling the squeeze; the entire cable industry is responding to the same broken algorithm by consolidating. That tells you the pressure is structural, not company-specific — which is precisely the kind of thing a bull case has to confront head-on, and which sets up the final stress test.

VIII. Bear vs. Bull Stress Test

Now let us do the thing every serious investor should do before forming a view: argue against ourselves. Put on the hat of a skeptical activist or a short seller, the kind of investor whose job is to find the soft spots in a story that the market is, this very morning, celebrating with a 22 percent pop. What would you challenge?

You would start where the accountability is weakest, which is governance. The dual-class structure that carries over into both new companies means that whatever value the split is supposed to unlock, Brian Roberts's grip does not loosen — he holds the same one-third voting control of each entity, with the same negligible economic stake.[^1]3 A skeptic's point is sharp here: separation is being sold as value creation for shareholders, but it changes nothing about shareholders' fundamental powerlessness. If either company underperforms after the split, public owners have no more ability to force a change of strategy, board, or management than they did before. You have unbundled the assets while leaving the control fortress fully intact in duplicate. For an activist, this is the ultimate frustration — the value-unlock thesis and the no-accountability reality sit side by side, and the second one means you can never insist on the first.

The second place a skeptic presses is the balance sheet, and specifically the question of how the debt gets divided. Comcast carries a substantial net-debt load — on the order of $82 billion — and the entire credibility of the separation depends on how that burden is partitioned between the two companies.2 This is not a neutral accounting exercise; it is a value-allocation decision with real consequences. The temptation in any media-versus-infrastructure split is to load the steady, cash-generative utility — the connectivity company — with a disproportionate share of the debt, in order to send the media company out the door with a cleaner balance sheet that the market will reward with a higher multiple. If that is how the partition is structured, then the connectivity shareholders are effectively subsidizing the media spinoff's valuation. A skeptic watches the leverage split like a hawk, because it determines who really bears the cost of the financial engineering. The early signal from the rating agencies has been one of stability — Fitch indicated it expected to affirm Comcast's investment-grade profile through the separation — but a stable headline rating does not answer the distributional question of which entity carries which obligations.11

With the skeptic's challenges on the table, here are the three key performance indicators that actually matter for tracking whether the bull or bear case is winning — and an investor should watch these and let the quarterly numbers, not management's narration, settle the argument.

The first KPI, for the connectivity company, is broadband ARPU growth versus net adds. This is the whole ballgame for the pipes. The bull thesis requires that price increases on existing customers more than offset the loss of subscribers — that pricing power survives even as the monopoly does not. The bear thesis is that you cannot keep raising prices on a shrinking base in a competitive market without accelerating the very defections you are trying to outrun. Watching ARPU and net adds together, quarter by quarter, tells you which force is winning.

The second KPI, for the media company, is Peacock and overall media-segment EBITDA — specifically, the path to sustained streaming profitability. The critical complication is that 2026 carries a peak of content spending, including a Winter Olympics and the launch of the new NBA package, which front-loads cost.[^3] The question is when, on the far side of that spending peak, the streaming and media operation crosses into durable profitability rather than perpetual investment. If Peacock's losses narrow toward breakeven as the content spend normalizes, the bull case strengthens; if the losses prove structural, the bear case does.

The third KPI applies to both companies: net debt to adjusted EBITDA. Each new entity has told the market a story of maintaining a conservative leverage profile — broadly in the sub-2.5x range — and the integrity of that promise, independently, for two companies that used to share one balance sheet, is the foundation of everything else. Leverage that drifts higher would signal that the separation strained the financial structure rather than strengthened it.

So how do the two cases net out? The bull case is clean and genuinely plausible. The separation succeeds in releasing the conglomerate discount. The connectivity company, once the DOCSIS 4.0 upgrade cycle completes and capital intensity falls, settles into life as an ultra-stable, high-cash-flow, high-dividend infrastructure utility — boring in the best possible way, with the highest barrier to entry in the entire economy. The media company, freed from the utility's gravity and energized by the parks, becomes a sought-after, pure-play entertainment franchise with irreplaceable IP and a theme-park empire — Epic Universe and all — that compounds for decades. Two focused, well-run companies, each loved by its natural shareholder, worth more apart than together.

The bear case is equally coherent, and a neutral observer must give it full weight. In this telling, the "remaining Comcast" is a structurally declining copper utility losing a technology war on three fronts to pure fiber and wireless 5G — a business whose pricing power has already visibly cracked, now forced to spend heavily just to slow its erosion. Meanwhile, the spun-off media company is set loose into the teeth of the streaming wars, compelled to overspend on sports rights and original content precisely as the linear cash flows that once subsidized that spending evaporate, with margins compressing rather than expanding. In the bear case, the split does not solve the two companies' problems; it merely makes each problem a standalone equity that the market can repudiate on its own. Both cases rest on the same facts. Which one comes true is an empirical question that the three KPIs will answer over the next several years.

IX. Epilogue & Outro

Step back far enough, and the Comcast separation is not really a story about one company. It is the closing chapter of an entire idea — the idea that bigger is automatically better, that owning both the road and the cars that drive on it confers an advantage no focused competitor can match. That idea built the great media conglomerates of the late twentieth and early twenty-first centuries, and Comcast was perhaps its purest, most successful expression: the cable operator from Tupelo that grew into a colossus straddling pipes, studios, news, sports, and theme parks. The June 29, 2026 announcement is the formal acknowledgment that the idea has run its course — that in an age when the consumer's attention is splintered across a thousand apps and the consumer's broadband can arrive over the air, scale and integration are no longer enough to win. Focus, the market has decided, is the new moat.1

The deepest irony sits in the people. The man brought back to run the connectivity company, Michael Angelakis, is the same disciplined CFO who, more than a decade ago, helped architect the acquisition of NBCUniversal — the deal that, more than any other, embodied the flywheel dream he is now returning to help unwind.[^1] The merger of connectivity and content, once hailed across the industry as the future of media and defended on earnings call after earnings call as a unique and durable advantage, is being dissolved at remarkable speed by the very team that spent twenty years assembling and praising it. There is no tidier emblem of how completely the strategic consensus has flipped.

What remains for the neutral observer is a set of open questions rather than a verdict. Will the conglomerate discount actually lift, or will it simply migrate onto two smaller companies, each carrying its own structural challenge? Will the controlling shareholder's undiminished, duplicated grip prove to be the steady hand the bulls credit it for, or the accountability vacuum the skeptics fear? Will the pipes hold their pricing power as the monopoly fades, and will the entertainment engine ever make streaming pay? The separation does not answer those questions. It merely splits them in two and hands each to a different set of owners. The great empire that Ralph Roberts began with 1,200 subscribers and that his son built into a $150 billion conglomerate is about to become two companies — and for the first time in a generation, the story of each will be told on its own terms.

References

-

The Death of the Telecom-Media Conglomerate — Wall Street Journal, 2026-06-29 ↩↩↩

-

Comcast Corporation Annual Report (Form 10-K) for FY 2025 — SEC, 2026-02-18 ↩↩↩↩↩↩

-

Brian L. Roberts SEC Form 4 Statement of Changes in Beneficial Ownership — SEC, 2026-03-10 ↩↩↩

-

AT&T Broadband to Merge with Comcast Corporation in $72 Billion Transaction — Comcast, 2001-12-19 ↩↩

-

GE Sells Remaining Stake in NBCUniversal Joint Venture and Related Assets to Comcast for $18.1B — GE News, 2013-02-12 ↩

-

How Comcast Outbid Disney in a Historic £30 Billion Blind Auction for Sky — Reuters, 2018-09-22 ↩↩

-

Comcast Completes Versant Media Group Spinoff — Nasdaq, 2026-01-05 ↩↩

-

Mike Cavanagh Amended Employment Agreement & PSU Grant Terms — Comcast Corp Form 8-K, 2025-12-15 ↩↩

-

Charter Communications and Cox Communications File Regulatory Merger Application — Federal Communications Commission, 2026-05-12 ↩

-

Comcast's Massive Epic Universe Theme Park Opens in Orlando — Bloomberg, 2025-05-22 ↩↩

-

Fitch Affirms Comcast's Stable A- Rating Following Separation Announcements — Fitch Ratings, 2026-06-30 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube